This Week In Petroleum (TWIP)

Posted by nate hagens on June 20, 2007 - 5:59pm

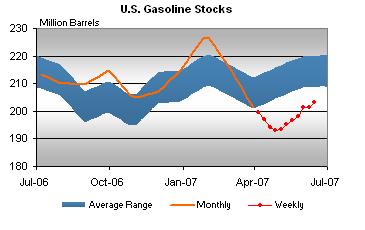

This morning at 10:30 am EST, the Department of Energy released their weekly supply reports for crude oil and refined products. Gasoline stocks increased for the 7th consecutive week, and the build of 1.79 million barrels to 203.3 million barrels was higher than the market expectation of a 1.19 mb rise. Gasoline prices initially sold off 2 cents, paused for a while, then dropped sharply and spent most of the day down 5-6 cents. In the last 30 minutes of trading however, the prices rallied back to finish only down 1.5 cents on the day. Crude, after being down $2 at one point, closed down 75 cents.

Robert is on vacation so I'm posting the text of the report for those interested, along with some comments from a prominent Wall Street analyst, Paul Cheng, of Lehman Brothers. The TWIP (the text that accompanies the data released at 1pm), and some thoughts below the fold.

THIS WEEK IN PETROLEUM (6/20) Original can be found here

Winter in June?

The 4.7-million-barrel (13 percent) drop in high-sulfur distillate fuel inventories between May 11 and June 15, could have some oil analysts wondering if the world has shifted such that we are now in the southern hemisphere, where it is winter time! These inventories are often referred to as heating oil inventories, since heating represents a major use of high-sulfur (500 parts per million [ppm] or greater) distillate fuel. The drop comes at a time when many analysts would expect heating oil inventories to be building for the upcoming winter season. However, high-sulfur distillate fuel is used for more than just heating oil, and this may explain why we have seen stocks fall in recent weeks.

As of June 2007, pursuant to Environmental Protection Agency (EPA) rules, fuel suppliers are no longer distributing distillate fuel containing more than 500 ppm sulfur for non-road diesel, locomotive, and marine use. (Some exceptions exist.) Instead, these markets are now supplied mainly with lower sulfur fuels. Using data from 2000 and 2001, EPA, during its rulemaking process, suggested that the markets affected by this rule represented more than half of the overall demand for high-sulfur distillate fuel. EIA analysts reached a similar result using more recent data from the 2005 fuel oil and kerosene sales.

The significant reduction in overall demand for high-sulfur distillate fuel strongly impacts inventory needs. Indeed, if desired inventories are proportional to demand, it would not be surprising to see half of the high-sulfur distillate fuel inventories shift to lower sulfur categories over some time period. This means that comparing high-sulfur distillate fuel inventories to historical data, such as a 5-year average, will be misleading, as the high-sulfur market is dramatically smaller now compared to recent years. Conversely, historical comparisons involving the combination of less-than-15 ppm sulfur and 15 ppm-to-500 ppm sulfur distillate fuel will also be misleading, since with more demand shifted to these markets, one would now expect inventories to be significantly higher.

For the time being, analysts seeking an undistorted perspective can focus on total distillate fuel inventories in doing any analysis related to heating oil or diesel fuel. As Figure 5 in the Weekly Petroleum Status Report indicates, current stocks of distillate fuel are in the upper half of the average range for this time of year.

Gasoline Prices Down, Diesel Higher

For the fourth consecutive week, the U.S. average retail price for regular gasoline decreased, falling 6.7 cents to 300.9 cents per gallon as of June 18, 2007. Prices are 13.8 cents per gallon higher than this time last year. All regions reported price decreases. East Coast prices dropped 4.6 cents to 297.6 cents per gallon. The largest regional decrease was in the Midwest, where prices fell 8.9 cents to 298.4 cents per gallon, while prices for the Gulf Coast decreased 5.9 cents to 290.3 cents per gallon. Rocky Mountain prices fell 4.4 cents to 318.1 cents per gallon but remain 33.8 cents per gallon above last year's price. West Coast prices were down 7.7 cents to 318.8 cents per gallon. The average price for regular grade in California was down 8.4 cents to 323.6 cents per gallon.

Retail diesel prices rose this week, climbing 1.3 cents to 280.5 cents per gallon. Prices are 11.0 cents per gallon lower than at this time last year. East Coast prices were up 1.1 cents to 280.0 cents per gallon. In the Midwest, prices increased 2.1 cents to 277.4 cents per gallon, while the Gulf Coast saw a rise of 1.1 cents to 275.3 cents per gallon. The Rocky Mountain region had the only drop in prices, down 3.0 cents to 290.7 cents per gallon. The West Coast price rose 1.7 cents to 295.8 cents per gallon. California prices grew 3.6 cents to 303.3 cents per gallon, but remain 15.2 cents per gallon lower than at this time last year.

Propane Inventories Sharply Higher

Propane stockholders reported sharply higher inventories last week with a 2.8-million-barrel gain that moved the nation’s primary propane supply up to an estimated 39.7 million barrels as of June 15, 2007. However, total propane inventories continue to lag prior year levels by more than 5 million barrels. Gulf Coast inventories posted the largest weekly gain of 1.8 million barrels, followed by the next largest weekly gain of 0.8 million barrels added to Midwest inventories. The East Coast was relatively unchanged while the combined Rocky Mountain/West Coast regions reported a 0.1-million-barrel gain during this same time. Propylene non-fuel use inventories edged up by 0.1 million barrels and accounted for a smaller 6.7 percent of total propane/propylene inventories from the prior week’s 7.1 percent share.

Paul Cheng, a well know energy analyst at my former firm, Lehman Brothers, had this to say on an afternoon research note:

"We think todays (6/20) DOE report was bearish for the petroleum complex in light of the more than expected buildup in total gasoline inventory, reflected in the 11% jump in imports. Although the market had expected utilization to increase this week, we are not surprised by the drop given the spillover effect for a wave of accidents from a couple weeks ago. However, we expect the utilization rate to jump more than 2% in the next weekm reflecting more than 400 m/bd of crude capacity that have recently returned to expectation. As a side observation, it appears the DOE may have overstated both the production, and correspondingly the implied demand on gasoline. We continue to hold a bearish view on refining margins and think that gasoline inventories could continue its counter-seasonal build of an average of 1-1.5 mmbls in the coming weeks, of which 500-600mmbls are attributable to finished gasoline"

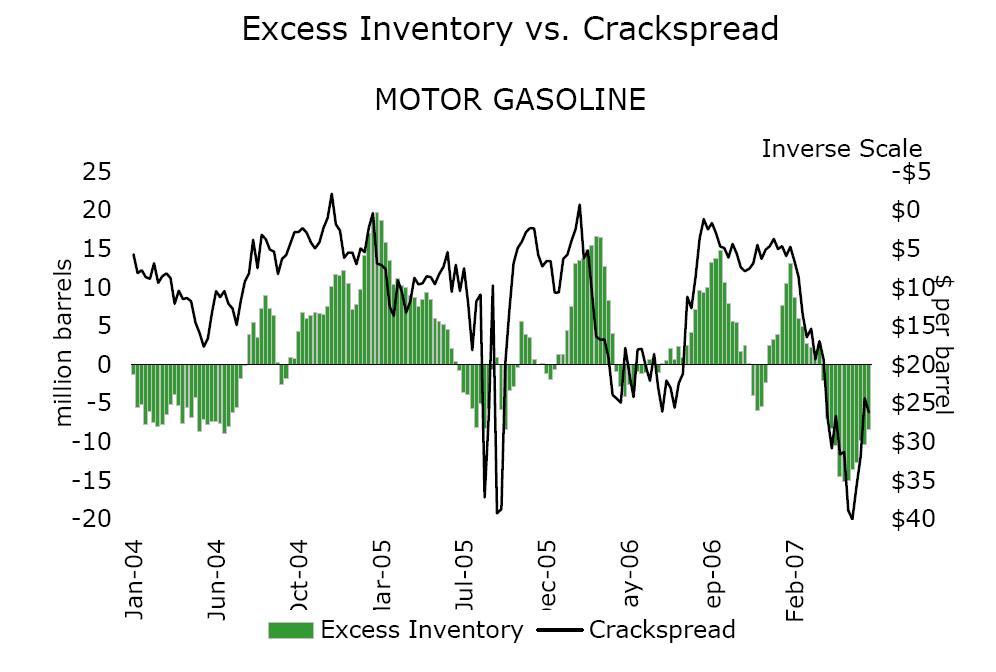

Crack Spread vs Inventories - Source - Paul Y Cheng Lehman Brothers Equity Research

In other words, the market is well supplied in the very short term, and since markets are efficient, this news incrementally should move oil and oil stock prices lower. The refinery issues from a few weeks ago resulting in near record crack spreads (gasoline - crude oil) seem to be resolving and the market should be returning to a more normal relationship.

After reading this, it all seemed very plausible (boring?), with the one exception that I was again struck by how our focus on the present is reinforced by the market mechanism. Traders base investment/speculation decisions on insights gleaned from how a 1 week update changes the previously accepted wisdom, a little bit at the margin, each week. If change (via the markets) is made through the summation of a bunch of tiny changes, I wonder how many of these one week updates in a row it will take, at some unknown date in the future, to significantly change the "previously accepted wisdom"?

On an unrelated, but interesting note, wheat futures hit an all time high today.

(Note: Here is the NYMEX crack spread calculator)

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

I continue to wonder what is happening in non-OECD countries: http://en.wikipedia.org/wiki/Image:OECD-memberstates.png

Can I fill my tank with "blending components."?

pretty much. Refiners hold bits and pieces separate to optimize their blending operations.

It's not that big a deal to move those pieces into finished gas.

"Crackspread" sounds obscene.

yea like toe jam...

Or...in my current position my long crack spread is exposed.

:-)

A very large build in total oil stocks.

------------------------------------------------------------

Total Stocks (Excl SPR) (7):

Week ending 06/15/07: 1,017.8

Week ending 06/08/07: 1,007.9

From the EIA weekly petroleum inventory report.

------------------------------------------------------------

A build of 9.9 million barrels of oil/products in one week

Sad day for oil bulls.

I read on peakoil.com that this might have been because oil that was being held in tankers offshore was offloaded this week. Not sure if its true but it makes sense.

It seems to ALWAYS be that there were tankers held in reserve to pump up the inventory numbers, so we can focus on that excuses instead of the fact that total imports are up over last year. Damn those pesky hidden tankers!!

It was announced that they would do this.

Here is the thread on peakoil.com

http://www.peakoil.com/fortopic28807-0-asc-270.html

They have a pretty good analysis each week.

Btw I don't think anyone expects the US to run low on oil until its in a serious bidding war with other wealthy countries for gasoline and oil. The problem right now is gasoline we seem for some reason to have allowed our gasoline stocks to drop dangerously low without bidding higher for imports. I think the reasonable glut in crude is a result of expectation that refinery utilization would be much higher than it is.

If you read back on the peakoil.com threads you would see that if we had been running our refineries at capacity we would not have a mini glut of oil like we do now. Next I suspect stocking up just in case there is a hurricane is also part of the issue. In any case the repeated inability to get our refinery utilization up is causing real problems in the market. We are seeing plenty of oil plenty of blending components but no gasoline. This means we will again have to bid on the world markets for gasoline imports leading to higher prices.

Outside of the unexpected deficiency in gasoline this summer I don't think anyone really expects the US to run out of oil or even run low this year and into next year. However I do expect us to be in a bidding war for real sometime next year. The problems this year are strictly related to refinery problems in the US. However the low gasoline stocks are a indication that we have to bid a fairly high price for gasoline imports this is a new event.

And finally the fact we can get gasoline for a price makes the OPEC claim of any sort of overall refinery capacity issue suspect since we have been able to get all the gasoline we want for a price without shortages occurring in the exporting countries. So looking beyond the local refining issues in the US we do see signs of peak oil caused by the relatively high bid price needed to attract gasoline imports. We should be at 4 bucks a gallon and importing gasoline like mad the fact we are not is setting the stage for possible shortages this summer esp if we don't get refinery utilization up soon. Especially if we have a hurricane that effects the refineries. This would force us to overbid in a sense on gasoline imports and could well lead to real shortages in gasoline if we actually have a shortage of refining capacity. Its worth watching.

The problem I have with your statements is that you, and you are not alone, fail to take into consideration the refinery upgrades that have been put into place over the last couple of years. There is a growing trend to 'cook' the oil thats left over after normal gasoline/diesel/jet fuel cracking to make yet more GDJ.

If we are squeezing another 6 gallons per barrel out at even half of our national refineries, then we need to utilize much LESS of our refinery capacity to produce the same amount of gas. This week is a perfect example of that concept.

Remember guys, 90%+ utilization is NOT normal, nor is it healthy! You will have a LOT of mechanical problems at that ratio. The only question I see today is how high will asphalt prices go.

Hmm we routinely hit 90+ in the summer months of peak demand.

So I don't think this is correct. I believe 93% or so is the norm during the summer driving season. In general you want to be at around 90% utilization if possible.

Next the coking is as far as I know for the heavy oils although I guess if you have one and are running light sweet you would also run a coker. I'd say configuring a coker for light sweet is fairly rare I'm not sure its even economical. The coker is to break up the asphaltenes in the heavier oil otherwise the yields would be much lower. Since we import a significant quantity of gasoline we can easily utilize all our refining capacity and still not meet demand.

You may want to read this to get a understanding of where a coker unit fits.

http://www.lloydminsterheavyoil.com/upgraderlaunch.htm

Notice they are using it only for heavy oils. The lighter grades can be cracked with other methods.

Finally this is Canadian refineries but you can see utilization above 90% is the norm not and exception as you claim.

http://www2.nrcan.gc.ca/es/erb/prb/english/View.asp?x=686&oid=1171

And last but not least you can google all this in a few minutes before you post so I don't have to debunk your statements.

And I guess you have not read my numerous posts on the increase use of cokers and the potential effect on asphalt prices.

If I recall, Robert stated that refinery utilization was in the mid 70's about 2 decades ago. So clearly it hasn't always been in the 90s as they have been these last few years. I guess 'normal' comes down to what time period we wish to define it by. I choose to look at trends that are just a 'tad' longer than 2 years or so :)

Memmel was correct.

http://tonto.eia.doe.gov/dnav/pet/hist/wpuleus34.htm

Utilization rates of over 90% are very common during the summer for the last 15 years. Its no where close to the mid 70's that you claim.

You're lucky RR is on vacation.

Where is the data for the years prior to 1991? 2 or so decades goes quite a bit further than you are letting us all onto.

http://dnr.louisiana.gov/sec/execdiv/techasmt/oil_gas/refineries/refinin...

Now, haven't we been through this subject before? Please, watch what you say :)

we added refinery capacity like crazy in the 70's when crude was $4/bbl and people thought crude demand worldwide would be 100 MMBD by now. Bad call. that left a ton of mangy capacity unable to compete once crude jumped up dramatically. That capacity remained operable, just utterly un-economic. They were units designed to make gobs of fuel oil for thermal electricity generation which made no sense once crude became expensive relative to coal or gas. Also their own energy efficiency was horrid as they were optimized for crude at $4/bbl. No payout for air preheaters, feed/effluent heat exchange etc at that low price.

No refiner will be happy with 70% op factor. They want to run full all the time as the last bbls are the most profitable since the fixed costs are already covered.

You claimed:

I presented you with eia data that shows 90%+ utilization is very much normal and has been for 15 years not the 2 years you claimed.

It is very clear that you were wrong.

I think there is a little disconnect here, Rethin. Perhaps you would care to actually READ the article that I linked? There is a wealth of information out there that shows we had far too much refinery capacity in the 70s and 80s. With the over capacity, margins were thinner, but a mechanical problem at one refinery wouldn't cause any systemic shortage of gasoline. What we find ourselves in today is a wonderful conundrum sponsored entirely by Big Oil's greed via shutting down a large number of our refineries in the past to shore up low profit margins.

So no, 90% is not 'normal' from an historical stand point. Perhaps its 'normal' in our Just-In-Time gas distribution system we now find ourselves in :)

You are clearly just trolling.

I don't understand why you think that, and I don't think that is fair at all. You seem to be the only person that is unwilling to acknowledge that we did utilize far less refinery capacity during peak months in the not so distant past. How sad that instead of examining the data for yourself you simply decide to engage in name calling.

nope. he's not trolling. You are clearly wrong.

Yes there was a period with a great deal of "operable" capacity that in truth never operated again. 70% OP factor is NOT in any way acceptable or normal. No refiner could make money like that. What you had was 12 MMBD of capacity that ran 85-95% of the time and another 5 MMBD in mothballs.

Hang on a sec here.

Perhaps you are confusing who's who here.

I, Rethin, am presenting evidence that 90+% utilization is normal and desired.

Partyguy, Troll, is claiming 70% is desired and the past 15 years of utilization rates are both unhealthy and not normal.

sorry. I'm with you 100% (well maybe with a 95% op factor) ) on this one. I question whether he's a troll though either. Pig headed I'll agree to ;).

lots of non technical people here with weird ideas of how the industry really works. And quite a bit of "don't confuse me with facts, my mind's made up".

By his comments here alone, I agree troll is a little bit of a harsh label.

But I think I know this guy by his MO. An old troll that went by the name hothgor. I suspect this isn't his only sock puppet either, but have no way of knowing for sure.

Also, reading though your comments I'm impressed with the depth of knowledge and experience you bring. Please don't be put off by the ignorance some of us show here (my self included unfortunatly). I'm sure I'm not alone in appreciating your input.

He is claiming this is normal its far from normal. 80-85% with burst above 90% is normal for most chemical plants. Most cannot even operate as low as 70% capacity the plant simply won't function correctly. I don't know about refineries in particular but I can't see them being much different from any other chemical plant I think they are fluidized bed reactors for their crackers from what I can tell these have to run at a certain load factor which is basically full or it does not function. The hydrogenation steps are also probably constrained to a load range. Cokers etc etc. It does not seem feasible to run a plant except at 80% plus capacity unless you take down a whole train.

we used to design for about a 60% min operating level when we could. Modern distillation equipment can do that. Some fixed bed reactors need enough flow to get a decent pressure drop to ensure everything spreads out -- don't want areas with no flow leading to coke balls etc. But you can keep gas recycle rates up at a cost in energy. I doubt there are very many fluid bed FCC's any more. They mostly used very short residence time reactor designs to maximize gasoline yield while minimizing gas yields. The regenerator side is still fluid but nothing keeps you from tweaking air rates up a shade. many plants have 3 X 50% pumps instead of 2 X 100% which makes turndown easier.

And I'll say again, the low op factors in the 80's came from many many ragged old plants not running at all and then being dismantled (see Wyden's list of dead refineries -- mangy old pieces of shit that were horrible neighbors, tiny tea kettles or just ancient and uneconomic). Those that were running were running with high op factors and throughputs as the refiners played "who will crack first and cut runs". The biggest and best never backed off (eg Chevron Pascagoula after their $1 billion revamp 1980-83). Terrible return on that capital, but with the costs suck, they ran full.

How far do you want to go back? 1600?

> seems to ALWAYS be that there were tankers held in reserve

I'm not really into conspiracy theories, but if, as RR has suggested, the peak coulda/shoulda been higher than 83 mbpd then is it possible that some "rogue" organization within OPEC is exporting oil on the side for their own private benefit? It could explain inventory conundrums.

Feel free to question the official number and don't believe the decimal places. I give them +/- 2mbd as my estimate of the accuracy. Nigeria and I'm sure Iraq export a reasonable amount of uncounted oil. In this case I believe the real numbers are probably higher than the official numbers. The down side is I suspect consumption in the producing countries is also higher than official numbers indicate. But you have to figure smuggling of finished products outside of countries that subsidize gasoline/diesel is big. Next people forget that in export land countries like KSA that are keeping exports constant are increasing production because internal demand is still increasing. Every day their spare capacity is eaten away.

it doesn't make sense and I'd want to see serious hard evidence before accepting this idea as anything but a conspiracy theory meme loved by those that think everything oilco's do is based on the dark side of the force.

IIRC oil is considered in inventory for EIA/DOE/API purposes if the shipment has been fully discharged and the figures set for billing purposes. Refiners don't report cargos currently being pumped. You just have to pick some rule and stick with it and it balances out over time. Considering we import 10 million bbls/day, even if you assume an average ship size of 1 MMBD that's 10 ships on the berth every day. It's probably more as the product tankers are more like 250 KB and some crude is taken off by lightering ships which are smaller in size.

Before you give into the conspiracy paranoia, keep in mind these ships cost $30K+ a day to park idle. The shipowners make more than than moving so they have no desire to just ac as floating storage unless they are on long term charter at a daily rate. Many ports/berths are controlled by government agencies. They move traffic to fit everyone's needs. They aren't going to play silly games for some trader. It's not impossible for a company to order a ship to only tender NOR (notice of readiness to discharge) to themselves and not the port facilities but it would be hard to jigger that to truly manipulate the weekly figures enough to matter. Moreover, anyone with sense looks at rolling averages to smooth out those sorts of swings and round abouts.

The majors don't own that much of the shipping anymore. Nor do any of the trade types. With diverse ownership of the vessels and pretty much transparent data on where ships are at any time available if you talk to a few ship brokers, it would be damn near impossible to hide a significant amount of oil on the water.

The whole idea is silly. But hey, it's a lot more fun to dream of star chambers and evil cabals.

I gave the link to the thread peakoil.com does not have a easy way to link responses.

http://www.peakoil.com/fortopic28807-285.html

And I'd like to add you don't have any reason to slam me I try to always provide links. You may not agree with my point of view but I don't troll I'm honest and I feel I've contributed. I don't agree with a lot of your comments but hopefully I'm not offensive. I was reporting what I read and the source. You don't have to shoot the messenger.

if I link to www.crazywankers.com will that count as a fact?

The whole idea is silly beyond words. Just because you have link from some site doesn't make it meaningful. You've link to rank speculation --"details are fuzzy"-- from an anonymous source without considering just where 19 MM bbls would actually sit. Can you/he even identify where one could could store this much oil? That's 10-15 VLCCs. It's not like you can hide them behind a bush. And it's not like there are 15 spare VLCCs you can take out of service to act as floating tankage. The day of old mangy rustbuckets available to do that sort of thing is over with the new pollution rules.

There's only 60 cts of contango to get you from now to Sept delivery. That won't even cover your TVOM so you'd have to eat all the demurrage on the ship or pay through the nose for tankage/double handling.

And to top that, you'd be stocking for a shoulder season when demand goes down. If you don't have a hurricane to bail you out by knocking out USG production, you could get a collapse like last summer. Whoo hoo. Lets store ice cream in summer for January too.

There is a bit of storage in places like St. Eustatius or the Bahamas but double handling is painfullly expensive. The Saudis used to do it back in the glut days but they don't have real world economics as the stuff comes out of the ground for free practically.

What I object too (perhaps too harshly, if so apols) is treating rank speculation as fact just because it fits your preconceived notions. A 6 MMB swing is fairly big, but not unheard of. It's only 10 hrs of US crude runs...You may well see a correction in next week's figures. Look at the rolling averages and don't try to see too much info in very sloppy figures.

Is Dow Jones in the same category as crazywankers?:

5/30/07 Dow Jones 20:22:06

Oil traders have been on a buying frenzy lately, with some even contracting with tanker companies to store crude offshore. One tanker broker said that three very large crude carriers, each capable of storing over 1 million barrels of oil, had been booked in the last week to hold crude off the U.S. Gulf Coast.

The premium enjoyed by outer-month crude futures to more near-term contracts, known as contango, has been driving much of the buying and storage, as traders expect the price of oil to rise over the summer.

The contango has only recently become wide enough to justify the storage of crude offshore, a crude trader said, noting that the contango narrowed on Wednesday.

see figures below. having dealt with the oil "press" I'd say no hopers might be more accurate than crazywankers.

Either I'm missing something not obvious or this is nuts.

Contango plays using floating storrage is not unusual. Nobody's hiding anything, the oil sits there until the carry play unwinds. It doesnt matter what the daily demurrage rate is, if the economics work they work. As for a ship earning more steaming than on demurrage not true. Although demurrage rates are negotiated each voyage they do not vary that much compared to voyage spot charter rates, so it entirely possible the demurrage rate is higher than the daily hire rate...and when a ship is chartered and the contango is there a short term floating storage option will be negotiated with the ship when it is chartered.

To think the trade/oil companies are using floating storage to manipulate stocks is nonsense.

I don't think anyone said it was to manipulate stocks just that it looked like a lot of oil that may have been held offshore was offloaded last week. The reason given was threat of hurricanes not stock manipulation. The only reason I brought it up was people where pointing it out as important.

If anything its just one more reason why US crude inventories are a really really useless number in a contango market.

Next of course if we actually did run low on commercial stocks we can do SPR draws until they are rebalanced ( at a price).

The problem is both KSA and the traders are using our inventory numbers as some sort of important indicator of how the market is supplied if they are low yes I can see that but if inventories are not low in the US I feel like they indicate nothing.

This seems true if you look at the widening spread between WTI and Brent even as US oil inventories remained high. Thus a well supplied US means nothing to the world market while a under supplied US is important since it means we could surge our imports. With the current situation the US imports are basically constant regardless of price.

What is important is gasoline imports and refinery throughput.

agree. floating storage is a typical technique. I guess myp point is you cannot do it in secret and then suddenly jam the bbls on shore in time to move a weekly DOE stats report.

But again people (Including Dow Jones) should put a bit of pencil to paper before repeating iffy claims.

Right we have a very mild contango. From Aug (Q) to Dec (Z) we have about $2 of contango to cover the 4+ months on NYMEX. so call it 50 cts/bbl/month.

This is wet oil so you have to pay for it. No margining here. At 6% interest that works out to 35 cts/month.

VLCC's are making about $40-50K/day (see

http://www.stockhouse.ca/mediascan/news.asp?newsid=7979351)

so for 30 days that's $1.4 million on 1.5 million bbls or almost another $1/bbl cost to store.

Add on vaporization losses (crude, like gasoline weathers in the heat of the caribs) Allow 0.1%/month or 7 cts/bbl/month

Just with these items I get about $1.4/month with only 40-50 cts of contango....small wonder "details are sketchy".

If you are just betting on rapid appreciation, you can bet for free on the futures exchange by just putting up a little margin.

I would not be surprised if they figured price would go up faster and are willing to take a larger short term loss gaming on a long term win. Now why take delivery at all is strange to me since you can do the same with futures contracts. Next floating storage is decommissioned tankers so your rates are high.

http://en.wikipedia.org/wiki/Floating_Production_Storage_and_Offloading

So the first mistake is that they are using functional tankers for the storage I don't think thats correct. I don't know the rates for real floating storage but it has to be much less than what your quoting since its used routinely.

Again since in my opinion the futures markets provide effectively the same profit margin without the hassle if a lot of oil is in floating storage its not simply their for profit reasons.

I still feel this site makes the exact same mistake as the MSM, specifically, the focus on the pieces of the pie rather than the size of the pie. For the MSM, this means one week the headline is more gas, the next week, more crude.

The total health of the US market can only be determine by the total. To this point, total inventories are again up marking six straight weeks. Probably more, but the data rolls off and I'm tired.

5/11 5/18 5/25 6/1 6/8 6/15

995,426 1,001,804 1,003,542 1,007,212 1,007,879 1,017,761

http://tonto.eia.doe.gov/dnav/pet/pet_sum_sndw_dcus_nus_w.htm

The lights may be out in Pakistan, but Bush Incorporated continues to motor along with a full tank.

What happened to Ganu and Oman? I haven't seen one mention since the crazy predictions of the Straights being closed for three weeks came and went.

jt

in my writing (and many others here) we ARE focused on the size of the pie. The above post, other than one commentary paragraph isn't about the content of 'this site', but a posting of todays government data and graphs with a quote from an energy analyst.

You speak to my only personal comment into this post, that the market (we) construe short term plenty with long term health.

I don't want to get too argumentative, because I really appreciate this site and the people like you who make it so informative.

That said, you don't know FOR SURE that oil production has peaked. My post above indicates that the oil coming out of the ground since the last extraction high of 2005 has been sufficient to keep OECD stocks (total) at normal levels and kept up with Chinese and Indian increases.

Until something tests the supply side and fails, no peak in my opinion. Today's report, and the last six, indicate that Supply has once again stepped up to the plate.

Since overall production worldwide has not increased someone did not get oil this year. Next OECD oil stocks are a lagging indicator of peak oil and we will be well past peak before we see actual oil shortages in OECD countries. If we peaked in 2005 I'm guessing end of 2008-2009 before we have dropped enough to start a bidding war between the wealthy countries and have resulting real shortages of oil. Note that instead of signaling peak oil shortages in the OECD countries signal that we are well past peak. I think your logic is flawed.

Next for the US we will probably suffer from not getting needed gasoline imports at any price well before we experience any sort of shortage of oil as countries refuse to ship gasoline and cause shortages in their home countries. So we will be in shortage conditions next year if the US/China/India grow as they did this year. In effect we will have a global oil shortage next year and this will be reflected in limited gasoline imports into the US.

This I expect to happen next summer.

In any case why would you expect OECD inventories to signal peak oil ? This does not make sense to me instead as I said they are the most lagging indicator of peak. The time between when OECD countries are having oil supply problems and TSHTF is probably a matter of months and certainly well past peak.

I'm a bit perplexed. We have been ranting and raving about how the steady climb in oil prices is a result of a bidding war due to Peak Oil, yet you come out and state that we have not been in a bidding war, and wont be until 2008-2009!? The 'wealthy' countries consume 60% of the worlds oil, and over 75% if you include the up and coming Fast Economic Developing Countries. I'm still wondering how big of a sample we need before we can confidently say that the worlds demand IS being met, if only for the moment.

Are you being intentionally obtuse?

"if we peaked in 2005 I'm guessing end of 2008-2009 before we have dropped enough to start a bidding war between the wealthy countries and have resulting real shortages of oil."

Any bidding war going on now is between the wealthy nations and the poor nations. For example look at Nepal or Senegal.

I'm surprised the poor were able to afford such high prices, especially with the oft quoted figures of less than a dollar a day to live off of. Clearly something else is happening, as I, nor anyone else, has all the facts. Lets stop pretending we do, shall we?

What in the world are you talking about?

Hi Partguy, first reply to you. News has been abound recently about shortages of energy in the 'poor countries'. On my count I've seen about on average one occurance every day of a shortage somewhere, be it petrol/diesel/electricity. The facts are starting to roll in. I think the point the others are making is that the bidding war with the poorer nations is well under way but above various thresholds the affordability diminishes in ever richer countries until it reaches the OECD countries.

Marco.

The news you are referring too is constantly tossed around here at The Oil Drum from one post to another. I have been searching for many months now to find ONE article that shows a country cant buy the oil they need that is NOT due to some political blunder. As of this moment, I have failed to find one.

You can take Pakistan, Zimbabwe etc off the list, as their problems are well documented and were years in the making and completely outside of the context of Peak OIL. I will be more than happy to discuss anything you do find in detail.

Not able to buy enough to keep the lights on, rather than none at all.

Dominican Republic and Indonesia (OPEC member BTW).

Indonesia endured blackouts because they could not afford the heavy oil for power plants, although they were waiting for new Australian coal fired plants to come on-line.

Despite problems in Nepal, at lower prices they could have afforded oil products. Combining higher oil prices with other problems and they went without.

Senegal.

Venezuela is keeping much of Central America going with concessions.

Alan

Another factor is even in the US many projects that use asphalt i.e. road building and maintenance are being delayed. Google and read various local stories its systematic across America as the high price of asphalt has slowed road construction. You have to figure that in poorer countries road construction has probably come to a grinding halt. World wide we have seen a tremendous amount of upgrading of refinery capacity to be of the complex form that includes crackers and cokers leaving less of the formerly cheap side products. In general the continuous upgrading of refineries to handle the heavier oils and even crackers to refineries designed for light sweet crudes has increased the per barrel production of gasoline and diesel at the expense of other products.

This shift to complex refining is helping delay squeezes on gasoline production but its coming at the expense of maintaining our roads and other uses of the low grade products that where formerly available from the simple refineries. So even in the US we are "robbing peter to pay paul". Bunker fuel supplies for shipping has been tight for several years now with shortages not uncommon.

Overall peak oil is felt in the poorer countries and with increased complex refining in supplies of the cheaper products asphalt bunker fuel etc that used to be readily available. The electric outages are often related to the fact that the poorer countries use oil fired generators for electricity production.

This is the current state of affairs post peak.

You can imagine that in the coming years bunker fuel shortages will put quite a crimp in the global economy.

Wall Mart won't get its cheap plastic crap from china if the ships are waiting to fuel.

Just to keep reminding people shortages are the Achilles Heel of the oil economy it turns oil powered equipment into big hunks of rusting steel. And you can imagine what electric outages does to factory production.

Give me one example of a ship entering port unable to stem bunkers because of lack of availability rather than a logistical snafu...

I'll answer because their is a flaw in your logic.

The reason is always logistical and will be until we are well past peak. Bunker fuel is freely traded and if supply is plentiful then you can stock up before you take a refinery out for maintenance. Same situation we have right now in the US for gasoline. On the surface its a logistical problem underneath its the fact we can't get imports except at premium prices.

Underneath this the reason is supplies are tight.

Underneath this you finally hit the real reason which is peak oil.

I'm certain people will claim its logistical problems right to the end we still have people that believe the US can increase production its just a logistical problem.

The question you have to ask your self is why are the storage tanks empty in all these places to cause tight supplies in the first place ?

If your serious then follow this story back.

http://www.bunkerworld.com/news/2007/05/67998

Why is their no bunker fuel in South Africa logistical problem right ?

Show me. I've been following bunker fuel now for about a year and I've seen persistent and chronic shortages to pop up world wide.

This is back in 2003.

https://www.oceanconnect.com/public/viewnews.jsp?articleId=6100

http://www.bunkerworld.com/news/2007/05/67990

Logistical shortages right ??

I think you maybe reading into my question a little too much. You mentioned the shortage of bunker fuel and by extention the disruption of trade flow " plastic crap...Walmart ... China ". I was asking for evidence this is so. In my experience I have never come across a ship knowingly entering a port and unable to bunker (ships usually order fuel well ahead of time)... It maybe they are unwilling to stem bunkers because of the price (they can get it cheaper elsewhere), or that due to some logistical problem, jetty out of operation or bunker barge out of action, they cannot get physical delivery.

If your argument is that supplies may not have been as plentiful as they once where that may have merit, as refineries have found ways to minimise their production of fuel and maximise their output of lighter ends.

It is also true that the price of bunkers are higher but that is not a real surprise since it is a derivative of crude which has increased in price. However if you look at the fuel oil cracks overtime since say the early mid 90's that differential has been steadily rising so fuel is actually cheaper as a percentage of the crude price.

But to say there is a shortage of bunkers which will impact on trade flows is erronous in my opinion.

Hmm a ship needs fuel to sail if it does not have fuel it won't sail. If it does not sail the cargo does not reach its port. To use my favorite example if its a cargo of oil drill bits or other parts for the oil business the drilling of a well is delayed. Less oil is available because of the delay leading to higher bunker prices and more shortages. Trade flows become increasingly erratic and the global economy slows. I gave a example of a direct feedback loop. But you can see that JIT inventory systems start to fail and we people begin to warehouse more product which puts them at a competitive disadvantage and increases the expense of doing trade or they endure empty shelves and lost sales. Worse I may travel to the store a few times in a row to discover the shelves are still empty before I get smart and call ahead.

The point is the tightening supplies and spot shortages of oil and oil products will directly slow the world economy without even factoring in price. Thus its acts as a first order natural case of demand destruction. Later on it will be the primary factor for demand destruction not price.

Its not clear to me which factor will actually be the largest demand destruction because of price even though the product is available or simple shortages. I'm leaning to simple shortages as the primary reason for demand destruction and I think high prices with product available is secondary. My assertion is we will have widespread demand destruction from shortages long before we have any significant price induced demand destruction.

This means people that have focused on price may be missing the mark. So if I'm right a lot of people are wrong.

And I think I'm right :)

Put it this way price is the noose tightening around or necks slowly strangling us. Shortages are 50 caliber rounds from a gun aimed at our heads. I think the 50 cal will win.

Thanks for the links to Bunkerworld.....However playing devils advocate you could no doubt go through Bunkerworld over the years and find numerous stories of supply disruptions. If the lack of fuel is because there is no crude to put through the local refinery at any price, or a lack of barrels to arbitrage in, you may have a point.

The short term tightness in supply at a given location is more likely from the late arrival of a the next fuel cargo or disruption at the local refinery than a systemic world wide shortage of fuel.

I believe demand is out stripping supply and it will continue to do in the coming years...demand will be reduced as alternatives become viable, and supply will be increased as hitherto uneconomic reserves come on stream. Will there be alot of pain and suffering in the meantime undoubtedly.

People here keep touting this coming or existing bunker fuel shortage. Silliest thing I ever heard. With the world's crude slate getting heavier and heavier and with refining investment lagging, there's no way we are truly short bunkers.

Now the price relative to crude may well rise. When I was one of the biggest blenders in the biggest bunkering port 380 cSt Bunker C was in the range of WTI - $4-7/bbl. that was when WTI was $15-20 and bunker went for $65-100/mt (6.35 conversion). We now have bunkers at $335/mt (say $53/bbl) with crude up closer to $65-70.

As a percentage of crude the price has narrowed, but this is irrelevant(another instance where ratios are a terrible to look at things). The spread has dropped. Why? because with gasoline margins at $20-30/bbl people are running their refineries as full as they can. the byproduct, bunker, is just a throwaway so to speak.

Sure refiners will eventually install upgrading to capture that spread. But all it will do is raise the price of bunkers. If ships need oil to move goods from A to B, they'll pay what it takes to get bunker fuel. And if you look at the profit in moving goods around relative to moving passenger cars around, we can easily afford higher bunker prices.

As to why tanked product may be thin. Who wants to sit on millions in inventory just to make life easy. The TVOM on 80,000 tons of bunker in tank (I had as much as 300KT at times) can be painful.

I hoped I made my position clear with the 50 cal comment.

I'll expand later in other posts. In short I'll reply to both posts with the key point your both missing.

Price will not be the cause of the end of the oil age its shortages. In fact the market will be unable to move fast enough to allow price arbitrage to cause demand destruction. It will be short swift and painful caused by shortages.

This means the price of oil and products is effectively infinity since its simply won't be available until the shortage is filled. This enforced conservation is how demand destruction will unfold.

The market will both lag in setting the price then way overprice or gouge in shortage regions until they get the products the need. This will cause shortages elsewhere.

This will happen with bunker fuel and they will get bad quickly.

Thats the argument I'm making and its important because it indicates that we actually will not get a lot of price warning before we enter into crippling shortages and skyrocketing prices. One moment your arguments are correct and the next I'm right.

The problem is seeing the pattern of rolling shortages that signal the system is about too break down. It will be quick painful and sudden. Price is not relevant to my argument.

When we simply physically don't have enough bunker fuel to fuel all the ships that need fuel someone will not get fuel regardless of price. We are in my opinion very close to this condition since I see indications of rolling shortages happening now.

Expand this to a number of rolling shortages moving around the globe and you can see the economic system effectively grinds to a halt quickly in less than a year.

Your free not to believe me but if I'm right you won't get a lot of warning before things fall apart quickly. So I'd suggest you take a long hard look at my argument since it implies collapse far quicker than even the biggest doomer anticipates.

Mexico oil production was down in May but exports were up. Was it that Mexicans cut back usage due to high prices?

Had to look at some more data and oil production for Q1 2007 was less than for Q1 2006.

Someone from Chevron was on CNBC talking about refinery problems. The sulphur removal equipment required to make low sulphur fuels has added more maintenance problems. It was like buying a car with alot of fancy options, more stuff that might break as the car gets older.

Some people were worried about oil company stock buy backs instead of reinvestment in drilling or refining. T. Boone Pickens used to launch proxy fights telling the stockholders the company was not doing enough for the shareholder and requiring stock buybacks. Companies had to fight expensive legal battles against Pickens, he was able to gain control of a few companies and the industry does buybacks to this day.

Mexico imports significant amounts of gasoline from the US so you would have to look at the overall balance to see if exports are really up. Probably all that has happened is more Mexican oil went to the US got refined and sent back as gasoline in short internal demand increased.

yeah. their refineries have always been pieces of crap with all kinds of operating problems. We were selling them gas in the 80's pretty regularly ex the USG and LA. Pemex is a prime example of why while Big Oil is mediocre at their business, don't wish for a govt run oil biz.

you're right. I don't believe this kunstleresque meltdown nonsense.

There have always (in my experience anyway) been periods when out of the way bunkering locales had shortages. The trander that supply these places cut things too fine often. Even big oil' bunker marketing groups were out at time is places like Panama when it was my job to help them out back in the 80's. They didn't want to stick their neck out and take big pieces in yet big pieces were all that wer economic. Otherwise your price gets too high relative to Rotterdam or Houston or LA and the ships fill up there and just haul it along. You can get concerned if you hear of shortages in Singapore, Rotterdam, Fujairah, Japan etc. If you are pointing to oddball locations like Capetown or the PanCan, maybe you should do a bit of research as to how often they had troubles in the past before anyone outside the industry much cared.

smacks a bit of "I'm right because I'm right". Any evidence beyond a few anecdotal instances and your gut?

I don't think Cape Town is out of the way as far as shipping channels go.

Singapore has experienced a lot of problems which I found disturbing.

As far as putting together a solid case most of bunkerworld.com is behind a paywall they have all the information but it costs. I've not found a free source with histories.

My example is not a gut feeling I think your misunderstanding.

Its a model for how depletion will play out.

The market obviously will take a long time to accept reality

so it will under price.

The consumer in general feels the same and will over pay or stretch thinking things will get better soon.

This leads to price spikes and shortages. These are well know to occur at the peak of a resource but its fascinating that they seem to be rooted in optimism.

So the real cause of demand destruction post peak won't be market driven the market will be effectively clueless for a long time increasing the price after the fact as they realize we have a new higher floor after each wave of shortages.

The key if you look globally is that increasing prices and more importantly competition for a scarce resource will result in constrained supplies and shortages.

These shortages will drive up price in a region eventually ensuring supply. During the shortage period we see fairly strong demand destruction from lack of product not price.

The key hear is a lot of the demand destruction is from simple lack of product not the ability to pay. The lack or shortage is caused by unwillingness to pay until forced not inability to pay this is driven by optimism that prices will come down.

Now we get into the musical chair situation. As each region experiences a shortage ups their bidding price and gets resupplied another region goes into shortage. So you end up with this wave of shortages moving around the globe underlying it is the lack of oil. As oil depletes they will get stronger and last longer and price increases will also work to eliminate demand. But the point is price is not a driving factor optimism that things will get better on the part of the buyers will trigger another bout of shortages as they are unwilling to "over pay". Most of the demand destruction is caused by the shortages themselves and the resulting economic impact. One more time Price is not important.

The problem is in a depletion scenario with all players willing and able to spend because demand is inelastic the price point for a stable supply is at infinity.

Think of it as a auction of the fountain of youth amongst the worlds billionaires allowing them to pool resources.

The value of the fountain is infinite but you will have a winner at a price even with a infinite value point. In our case its more important that we have a loser and because of globalization the economies of the winner and looser are tightly linked.

This is not a gut feeling and it CRITICAL sorry for the caps for understanding how oil depletion will play out. Assuming demand destruction is caused by price alone is not correct and its a minor lagging part of the model.

I'll post more on this later.

I don't think Cape Town is out of the way as far as shipping channels go.

Singapore has experienced a lot of problems which I found disturbing.

As far as putting together a solid case most of bunkerworld.com is behind a paywall they have all the information but it costs. I've not found a free source with histories.

My example is not a gut feeling I think your misunderstanding.

Its a model for how depletion will play out.

The market obviously will take a long time to accept reality

so it will under price.

The consumer in general feels the same and will over pay or stretch thinking things will get better soon.

This leads to price spikes and shortages. These are well know to occur at the peak of a resource but its fascinating that they seem to be rooted in optimism.

So the real cause of demand destruction post peak won't be market driven the market will be effectively clueless for a long time increasing the price after the fact as they realize we have a new higher floor after each wave of shortages.

The key if you look globally is that increasing prices and more importantly competition for a scarce resource will result in constrained supplies and shortages.

These shortages will drive up price in a region eventually ensuring supply. During the shortage period we see fairly strong demand destruction from lack of product not price.

The key hear is a lot of the demand destruction is from simple lack of product not the ability to pay. The lack or shortage is caused by unwillingness to pay until forced not inability to pay this is driven by optimism that prices will come down.

Now we get into the musical chair situation. As each region experiences a shortage ups their bidding price and gets resupplied another region goes into shortage. So you end up with this wave of shortages moving around the globe underlying it is the lack of oil. As oil depletes they will get stronger and last longer and price increases will also work to eliminate demand. But the point is price is not a driving factor optimism that things will get better on the part of the buyers will trigger another bout of shortages as they are unwilling to "over pay". Most of the demand destruction is caused by the shortages themselves and the resulting economic impact. One more time Price is not important.

The problem is in a depletion scenario with all players willing and able to spend because demand is inelastic the price point for a stable supply is at infinity.

Think of it as a auction of the fountain of youth amongst the worlds billionaires allowing them to pool resources.

The value of the fountain is infinite but you will have a winner at a price even with a infinite value point. In our case its more important that we have a loser and because of globalization the economies of the winner and looser are tightly linked.

This is not a gut feeling and it CRITICAL sorry for the caps for understanding how oil depletion will play out. Assuming demand destruction is caused by price alone is not correct and its a minor lagging part of the model.

I'll post more on this later.

Hi memmel,

An aside, I saw the photo of Sharon; I appreciate your sharing it.

re: "I'll post more on this later."

I feel these points in this thread are critical, and very much worth further discussion.

Is there any possibility you might gather your thoughts and write up as a short article for a future main article?

I'd like to see this scenario benefit from some productive discussion.

I'd like to see Hirsch and others have the opportunity to see it, as well.

Thanks for your thoughts on my daughter.

I emailed this thread to WT Khebab and Stuart and reposted a synopsis on the Ghawar thread over in the EU oil drum site.

I'd like to see if they are willing to critique the idea.

I'll try and rewrite it some and send it to you if I don't get a response from them in the next few days.

I'm not clear on the best way to plug in numbers for the concept. The simple way to apply numbers is to assume a 500,000 bpd decrease results in 100 5000 bbd shortage conditions world wide. Hopefully I'll get some feedback.

But you can see how a 100 small events moving geographically can be lost this can continue until the system is actually quite unstable before the full extent of the problem becomes obvious.

Hi OilCoEx,

Interesting to hear your views, (and hope you'll reply further to memmel's post below).

Meanwhile, I'm curious...

re: "I don't believe this kunstleresque meltdown nonsense."

I'm wondering...

What *do* you believe?

What scenarios seem most likely to you?

How do you see decline playing out?

How do you see the evidence for past "ELM" behavior affecting the scenario (WT and Barlett's) for exporters supplying less to the world market?

And what else do you believe or see or think about, in terms of scenarios?

most of africa as well as pakistan.

i agree to ignore Zim

what about Ghana?

pakistan doesn't have enough money for its FF oil burning electricity generation.

i fail to see how this "years in the making".

Pakistan has a problem with rapidly increasing demand coupled with a lack of investment in electrical generation. It's the same problem that MIGHT hit the UK in the next decade, and MIGHT hit the US, but those won't be related to PO, more so to gas production.

jteehan

i can only speak for myself, but in the thousands of comments ive made on this site, ive never predicted when I thought peak oil would be, other than a broad range. To persuade people that a major paradigm shift is needed - it doesnt really matter if its 2007 or 2011 or 2015- big changes are coming - I hope we have more time.

What does matter is that we dont look at higher and higher prices (like we are now) and look at higher production (like we are now) and say - 'oh its some other factor causing prices to go up', while forgetting to notice that the gross production includes products either with fewer BTUS (ethanol, NGPL) or stuff that uses more energy itself to refine. In other words, the definition of 'oil' and 'peak' themselves are going to be shifty.

The net matters

Gonu is the storms name. It seemed to have a real effect I was going to comment on after Gonu the floor price seemed to increase from around 64 to 68 a barrel for WTI. This increase happened post Gomu and was consistent this Nigerian strike has ruined any chance to track the even in isolation as far as price goes we will have to wait for monthly production numbers to see if their was any effect on production. As far as I'm concerned it did seem to have a real effect on oil prices. Not too 70 as I thought but it did seem to move the floor price up from 64 to around 68 a barrel. I notice its not going below 68 so far. I wish we had had more time before another above ground event but ohh well. Lets see if prices drop below 68 for any length of time. I think what we will see going forward is prices increase for each event and then come to a new higher floor.

So to me the key going forward is the floor price will keep increasing as events cause prices to increase they will not return to their previous lows. If your looking for depletion effects on oil prices I feel the minimum or floor price is far more relevant than the peak prices. It seems that we are rapidly closing in on a floor price of 70.

The price is up in dollar terms. Strip out the 30% drop in the dollar and you're back to the mid-forties. Three percent inflation a year is $1.20 a year. Of course prices are rising, demand is up.

Milk is way up too. That doesn't mean we're at Peak Cows!

When I was 18, I made $9600 that year in the Navy. I drove an old hybrid Chevy PU with a leaky 327. I say hybrid, because it burned as much oil as it did gas. Gas was $1.50 a gallon. I drove everywhere.

Sadly, it's 25 years later. I made almost 20 times that number last year. I drive a Prius. (and a 24000 lb Motorhome with a CAT C7 diesel). I have a 3000 watt pv array on my roof. The percentage of my check expended on energy has dropped by 98%

There's going to be a huge recession starting this year which should push out the peak by a lot. Or, even if 05 was the peak, we won't know it until the recession ends.

Or Plan B, my motorhome has PV on the roof and an inverter. And the bullet holes from the angry mobs will make for nice ventilation in the summers.

Hey, my daughter was born with severe brain damage. Just exactly where do you think peak oil rates in my list of things to worry about?

First the effective of the storm is determined in relative dollars adjusting for inflationary effects or normalizing does not make a lot of sense for this particular problem. Its a short term relative measure. And all I'm saying is it did seem to have and effect but the Nigerian issue now clouds the signal. Its impossible to tease out the relative effects of multiple above ground issues.

I'm sorry to hear about your daughter I've lost both a younger brother and my own daughter so I can understand your pain.

I don't know if your in financial duress but my father manages a fund to help critically ill children in memory of my daughter. Its restricted to Arkansans but he would probably be willing to help you find something similar in your area if you need it.

http://www.arkansas-cares.org/baby-sharon/

Next if things get as bad as I think they will I'll try if possible to do something for children with special needs.

I've talked with my dad quite a bit about peak oil and you may want to network with him on this issue its important to try and keep our humanity no matter how bad things get.

My email is public and my father is well settled in the Little Rock community so feel free to contact me any time in the future and if I can help I will.

Hi jtheehan,

Thanks for your comments, and I'm glad you're contributing here despite the obvious stress your family must experience (for which you also have my moral support.)

re: "The percentage of my check expended on energy has dropped by 98%".

To do a whole analysis, perhaps you'd have to look at things like the price plus operating cost of the Prius, wouldn't you? In any case, AFAIK, the energy use per capita (US) has increased, so direct energy/power costs (home utilities, gasoline, etc.) taking a lower percentage of your income makes sense. (Or, memmel can correct me :))

The somewhat opposite question, though: What is the relationship between "increasingly cheap energy" and "peak oil"? Are you saying that "peak" (or impending decline) requires a gradual run-up in oil price? As an indicator?

Deffeyes and others have predicted increased volatility as we approach peak, and I believe Stuart has made one of his graph, which illustrates this exact occurance.

re: "...recession pushing out peak". Could you please expand upon this and explain a little more? I'd like to understand your point.

With refinery utilisation down, what has allowed a gasoline inventory rise? Is it reduced consumption, increased imports, or both? If imports are rising, is any country having to make do with less?

You can find the actual numbers here:

http://tonto.eia.doe.gov/oog/info/twip/twip_gasoline.html

Gasoline demand was up but so were imports... but I would remind everybody that these measurements are always open to later revision. As with all similar measurements, there are systematic and random measuring errors, and the EIA has some write-ups on their site wrt methodology.

Actually,

The finished gasoline numbers were down.

Interesting to me anyway, is that the RBOB with Alcohol accounts for ALL of the increase listed under gasoline this week.

Jet fuel was down by a million as well.

At the moment I'm completely perplexed by the way the market is behaving you would think that we would have kept prices high and imports high until we had a reasonable cushion but thats not the case its like the market has decided that we are going to experiment with finding our real minimum operating levels.

Its almost insane to trade a few cents off now in exchange for major problems later if we have a hurricane. I don't understand but my gut tells me we will pay dearly for this market decision later this summer. I'd rather see 4 bucks a gallon now than spikes over 6 and shortages if we have a storm. Basically from what I can tell if we have a decent hurricane we will see widespread shortages throughout the country before we can get the imports to make up for lost production.

Crazy.

This is the problem with free markets, they don't plan ahead. Remember all that stuff about discount rates? Traders will rather make a definite 4 bucks now instead of taking a chance of making 8 bucks in 2 months time. At least the vast majority do, there are a few making long term plays, but not enough to make a difference.

Markets are good at short term resource allocation, but lousy at long term strategic planning. There is no intelligence in markets, so you can't call it crazy, it's just a feature of the way they work.

Yup.

Capitalism is a heady brew of relative fitness, steep discount rates, and a species that has the technological means to extract resources outside of their local environment, concentrate digital and ostensible wealth, thereby creating carrots (drive) for the rest of their steep discounted, competitive tribe. The market is the carbohydrate that keeps it all going.

This is how I think when I just wake up and haven't had coffee. Im lucky to even have a girlfriend...;)

And notice Mr Hagen's remark about record wheat price.

The 19 degree Freeze in April did a number on Arkansas, Kansas, OK, wheat.

And the largest producing Ozzie state will be at least 10% less than predicted.

They'll cut to 20 million tons from 22.1 May est. IMHO.

Arkansawyer

I agree fully, however I have never experienced a decent Hurricane!

Prices are a function of people trying to make money, not preparing for a problem. Problem solving is not included in their job requirements.

An Arkansawyer here.

I haven't been posting at TOD since Katrina.

I've been reading almost daily since but I've wanted to see how events would play out.

And I was having trouble getting on with my acct as well and didn't feel like making an effort. 8D

But you touched a nerve Memmel.

You and WT, and a couple others on this post.

I'm in Ag in E Arkansas and have a Plan B,C, and D.

Plan A is in NW Ar. Nutt sucks BTW. Broyles should be gone yesterday And Malzahn

will do well at Tulsa IMHO.

But back to PO.

There's a 36 inch pipeline planned between Bald Knob and Helena to gather Fayetteville Shale gas.

It'll be interesting to see how this progresses.

Broyles is GONE ?

Sorry this is big news :)

I've talked with my dad a bit about Arkansas first you can get incredibly rich delta land cheap throughout the state so farming is not and issue the population is low. Surrounding and in the state is a fair amount of NG production. Plus it has a nuclear reactor that formerly supplied a lot of electricity to New Orleans not sure whats happening their. My uncle is a engineer for the electric company APL ? And he said the loss of population in New Orleans was a real blow to the regional electric company.

The only caveat I have about Arkansas and the lower Mississippi delta region in general is the large number of people with little education and lots of guns. I think things will get a git tense in the region when Jim Bob can't get gasoline for his 4X4 and trying to get creationist to switch to renewable fuels is a tough business. But seriously outside of this the entire region probably is the richest region in natural resource in the world Oil/Gas/Timber/Crops great waterways and low population. In the cities at least the education level is high and their are still a lot of skilled metal workers most probably in the oil industry right now.

My family is dealing with the Nature Conservancy now.

There is no more land between Searcy and Helena for sale w/ the mineral rights intact.

The Game and Fish just bought Stuttgart land for $9000 +an acre.

Any farm land now is a bargain for less than $2500 per acre.

APL is now Entergy which left NO for Clinton MS after Katrina.

And how did you know that my buds call me Jim Bob?

8D

it's not crazy. Just very short term thinking by the trader types that really do set the marginal price. There is no overarching force willing to take a loss to provide the price insurance you are looking for.

Go look at the NYMEX gasoline prices. Why would you stock bbls now when they are worth less later if you look at the forward curve. We've already had a bit of stock building as evidenced by the 1st month/2nd month futures dropping from about 15 cts down to 7 ish. If we have another hurricane free August, you could see the same puke out in gasoline as last year with people liquidating their emergency stocks as we head into fall.

always keep in mind that the market has the attention span of a 5 year old and the planning ability of the average building contractor (ie long term planning is what's for lunch?).