| Is "shale oil" the answer to "peak oil"? | The Oil Drum | Oman’s unrest may be a domino, not just to suppliers, but also to customers |

Tech Talk - Countries producing around 2 mbd - Nigeria, Angola, Libya and the UK

Posted by Heading Out on March 6, 2011 - 6:47am

The growing concerns about the stability of the countries of the Middle East and North Africa (MENA), because they make significant contributions to world oil supply, adds additional meaning to these weekly posts on the world’s major oil producers. To briefly recap, I looked at the top tier oil producers as listed by the EIA (i.e. those who produce more than 3.1 mbd in 2008) in the first post of the series. (These were Russia, Saudi Arabia, the United States, Iran, China, and Canada.) In the second I looked at the next four countries on the list, namely Mexico, the United Arab Emirates (UAE) Kuwait and referred to Venezuela – subject of a series of posts earlier in the year. The third post covered Norway, Brazil, Iraq, and Algeria. And so now we move on to look at Nigeria (2.35 mbd), Angola (2.0 mbd), Libya (1.87 mbd), and the United Kingdom (1.58 mbd). The numbers in parentheses are the production numbers cited by the EIA for 2008. To put these countries in greater context, these take us down to number 18 on the list, and with one more post I will have covered all the countries that produced more than 1 mbd on average in 2008.

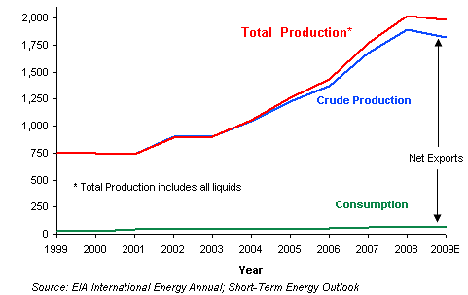

I will start with Nigeria, which now is cited as producing 2.4 mbd of crude and condensate in January 2011. The country has been having considerable trouble with sabotage and internal unrest that has had a negative impact on production. However, the country signed an Amnesty Program with militants in 2009, which has reduced disruption. As a result, in February Nigeria was able to raise production to 2.6 mbd. If this can be sustained it will bring production back over the peak level that was achieved back in 2005.

Note that for crude oil production alone, Nigeria is listed as producing 2.17 mbd in January, according to the February OPEC MOMR. (Which is also a gain from the above chart). In light of some of my recent comments on who might be hurt if oil production in some of the MENA countries drops off, it is perhaps interesting to note which countries got oil from Nigeria in 2009.

Historically Nigeria flared much of the gas that was associated with the oil, particularly in the Niger River Delta, where much of the oil is found. That practice led to some of the more dramatic stories that came from the region, before the amnesty. There is, however, a concerted effort now to capture and market this natural gas, as well as supplies that come from gas wells in the country. This has led to some optimism by the Government over future sources of revenue.

The Minister also disclosed that the establishment of two new Liquefied Natural Gas, LNG plants, in Olokola in Ogun/Ondo States and Brass LNG in Bayelsa state, will create over 7,000 jobs and inject over $1 billion into the host communities.

There are a total of 6 LNG trains at Finima, on Bonny Island, first coming into production in September 1999 and supplying a variety of customers. While the capacity is at 1.1 Tcf, recent figures have been at about half that volume. (And this is about the same volume that continues to be flared in the country.)

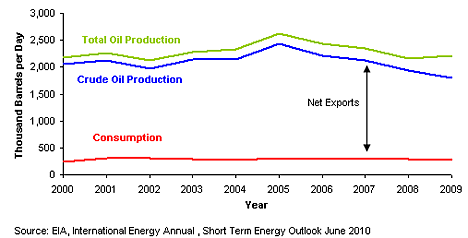

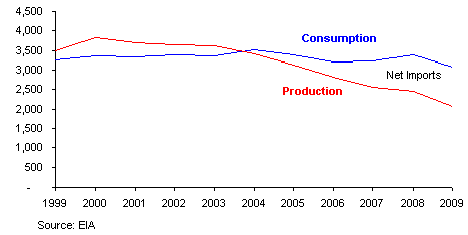

With Nigeria having increased overall production since 2008, though potentially having limited potential for much greater increase, the next country down the list is Angola, which since 2007 is also in OPEC, and OPEC list the January Angolan production of crude at 1.62 mbd. This is significantly below the overall 3.8 mbdoe that BP has reported for total energy production in 2010. Because of some technical problems with water injection used to help move oil from the reservoirs, moves to address the problem might reduce the overall average for 2011 to 3.4 mbdoe. Angola exports about 1. 7 mbd of oil, but is responsive to OPEC requests to control production in order to keep prices at the OPEC comfort level. (Which has risen from around $75 to over $100/bbl in the last few months). Thus the declines shown in the EIA plot below, which only shows through 2009, are more politically induced than due to geological conditions. The EIA, for example, lists projects for this year alone that are expected to add 650 kbd to production, and likely export. Unfortunately we are now far enough down the list that while these numbers are significant in their own right, and for the country they may not give that much help to the overall shortages that may evolve over the next year.

Angola currently is building an LNG project at Soyo, expected on stream in 2012 which will handle around 1 bcf/day. Apart from the LNG, which will be exported, the plant will send some 125 mcf/day of natural gas into a distribution network for domestic consumption. Until the plant comes on line, most of the almost 1 bcf of natural gas that is produced every day is either flared or reinjected to help with oil production.

Trying to project Libyan future production is rapidly becoming meaningless, I fear, as the initial moves to remove the current Leader have not met with sufficient success to eliminate the possibility of civil war. It was only a few weeks ago that Libya was producing at around 1.6 mbd of oil, and Luis de Sousa has reposted an earlier review of the past history of their production. He presciently notes in that post that the rising population of the country is going to demand more of the resource be spent at home. The topic of Libyan production will likely continue to appear in other posts – as it just has – but at the moment it appears, for a variety of reasons, that the system is effectively shut down.

Little if any oil can be shipped out of Libya because most ports were closed. Meanwhile, storage tanks were filling up rapidly. Oil traders said one major oil company cargo ship was supposed to berth this week, but no one was at the port to deliver an oil shipment, and shipping companies were reluctant to send ships into the Libyan ports.

I have also discussed elsewhere the likelihood of sufficient increase in production in other countries to make up the shortfall. Gazprom has been helping Italy, for example, and Saudi Arabia is increasing production, but how long this will last, and how much will ultimately be needed remains an unknown. It really depends on how many dominoes fall, and how long they remain on the table.

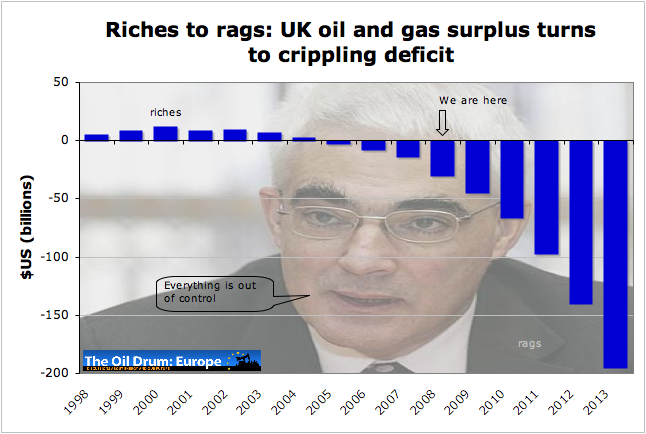

Which brings us to the United Kingdom. Back in the troubled days of the first oil shocks some thirty to forty years ago, it was the combination of new production from the fields in the North Sea and the North Slope that helped bring oil prices down to the low level which allowed the years of growth until now. But we have reached a point where those resources are beginning to disappear, and the UK has turned from an energy exporter to a growing importer. Euan Mearns has documented this progression in a much more detailed and better way than I illuminating, for example, back in 2008, the coming seriousness of their problem.

If we look at the situation today, the reports for last year note:

In 2010, the UK produced 850 million barrels of oil and gas equivalent (boe) or 2.3 million boe per day. Current plans now target reserves of 11.6 billion boe, 1.3 billion boe more than was anticipated a year ago, reflecting the outcome of increased exploration and appraisal activity across the UKCS and particularly West of Shetland. Oil & Gas UK believes there could be up to 24 billion barrels of oil and gas still to recover from the UKCS.

This was about 60% of the UK energy need. Production of crude for last November was 1.047 mbd from offshore, and 9,344 bbl from land wells. The natural gas numbers were 2.7 Bcf from offshore oil wells (as associated gas) and 2.8 Bcf from offshore gas wells. In addition there was some 12 kbd of condensate from the offshore gas fields.

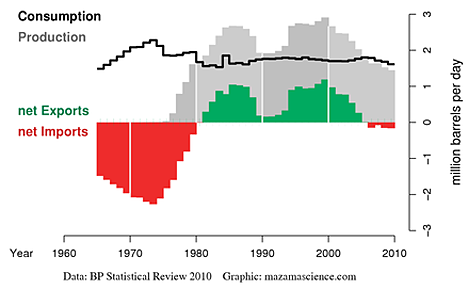

Whether one uses Euan’s plot, or that from the Energy Export Databrowser:

The UK is clearly entering a more expensive future as it must find more oil from overseas, just as that supply is tightening.

On the other hand, while the situation is getting somewhat worse more rapidly with natural gas, as the EIA plot below shows (and it contributes to Euan’s total figures) there is a sufficient glut on the world market at the moment that there will not be that immediate a problem in the short-term.

The energy situation in the UK is becoming recognizably more dire, and the Secretary of Climate and Energy, Chris Huhne has just pointed out that the price of $100 a barrel for oil justifies a greater investment in green technology:

Drawing on research conducted for the previous government by Lord Stern, Huhne argued that a $100 a barrel price is the exact point at which the economics of climate change pivot so that it becomes cheaper for British consumers and businesses to invest in green technology than remain with the status quo.

He said that if oil only reaches $108 a barrel by 2020 as predicted by the US Department of Energy, which would also lead to higher gas prices, then "the UK consumer will win hands down". He said the UK consumer would be "paying less through low-carbon policies than they would pay for fossil fuel policies".

This does not recognize that most renewable energy technology currently focuses on generating electricity, while the crisis is in liquid fuels for transportation. It also ignores the likely oversupply of natural gas, which is a separate price from the rising price of oil over the coming years. Tsk!

The current situation in the MENA countries is in such a state of flux, and the impacts barely recognized as yet, that it is becoming even more difficult to have any confidence that the predictions of performance that were being used only a couple of months ago will continue to have much validity in predicting what is likely to occur even in the relatively short term future.

Tech Talk - Countries producing around 2 mbd - Nigeria, Angola, Libya and the UK

PDF version

13 comments

Tech Talk - Countries producing around 2 mbd - Nigeria, Angola, Libya and the UK

PDF version

13 comments

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

Is anyone familiar with the technologies used in Libyan oil fields? Libya is at or near the midpoint of depletion

23/2/2011 Quick primer on Libyan oil

http://www.crudeoilpeak.com/?p=2621

so modern technology is needed to get the 2nd half of oil out of the ground. With so many weapons around in the country it is doubtful whether foreign oil workers will return in the foreseeable future.

The question arises: will the oil fields be damaged by not producing, e.g. oil moving into pockets of rock where it is difficult to extract? Any timelines involved?

Matt - Not much potential for the reservoirs to be damaged directly. There can be a problem with the well bore and surface equipment with an extended shut it. But still more an inconvenience than anything else. Some EOR methods can lose significant efficiency if shut down but I have no details on such ops in Libya. Actually more damage to the production equipment can occur when they put the wells back on especially if it's done by unskilled folks. But again more an inconvenience than a catastrophy.

I'm wondering if anyone knows the lie of the oil lines in Libya. I saw this just now on the BBC live blog:

I know there's oil over in the rebel-controlled East. Does this oil supply Tripoli? If so, wouldn't it make sense to cut off Gadaffi's supply? Additionally, why would the rebels be running out of oil if they hold the main supply - can they 'tap' into oil lines and divert it for their own use?

Edit: Ah, sorry just seen the link above to the oilfield map: http://www.crudeoilpeak.com/wp-content/gallery/libya/libya_oil_gas_field...

Hmm, so if the rebels are occupying Ras Lanuf, why do they fear an oil shortage? Or has Ras Lanuf ceased all operations?

First of all, the rebels issue is a fuel shortage. Doubtless a limited amount of Libya's crude oil production is refined in country for domestic use. Also, right now the rebels are a pretty rag-tag bunch. They are mostly heading out to the front-lines trying to be heroes, with few of them joining a logistical effort to bring fuel with them. So they are probably depleting the supply of refined products that are already near the battlefield, although I guess it's anyone's guess how much stocks there were to draw from and how much is still left.

Ras Lanuf almost certainly has ceased all operations during the fighting in the last 48 hours. And if any part of the refinery was damaged, it may not resume operations soon. The same is probably true of Marsa-al-Brega. It would be interesting to know whether Gaddafi's air force has tried to disable the refineries to prevent the rebels from benefiting from them, or whether they've left them alone in the hopes of recapturing them.

Judging from the map, the rebels seem to have three options to fuel an advance beyond Ras Lanuf:

1 - Get refining in Ras Lanouf and/or Brega online.

2 - Ship crude to Benghazi and truck refined products back.

3 - pipe crude to Tobruk and truck gas all the way back.

None of these appear easy. The Libyan air force, if it is in the air, could easily nix any of these options (say, by bombing the pipelines in the middle of the desert) without worrying about the propaganda cost associated with killing civilians.

Thanks for that. Looks like a fragile situation. I saw some estimates saying they only had about 8 days worth of supplies. I wasn't sure if that was fuel, food or what.

I guess this is why they appear to be pressing on towards Sirte and Tripoli.

From a rebel's point of view I imagine they'd want to be targeting Tripoli's supply from the Al-Hamra fields. There has been pretty intense fighting at Zawia with Gadaffi keen to retake it, so I guess that's indicative of its importance.

Thanks for the summary David. I just wanted to point out that we have an additional databrowser set up specifically for studying Gas Trends. It provides access to both the BP and IEA data on natural gas and thus a more complete set of nations from the IEA data. I find the full historical chart for UK natural gas trends to be much more compelling than the IEA's chart which inexplicably only begins in 1999. Here's the full story of UK gas production.

(We hope to have the EIA oil data up and running in a databrowser by this summer.)

Happy Exploring!

Jon

I have Oil Shock Model results for many of the countries involved in HO's series on second tier suppliers.

see "The Oil ConunDrum" Google Docs treatise.

England, Norway, Mexico, Libya, etc.

These were mostly based on circa 2004 data so you can see how they are panning out. Modeling of his sort has proven very useful IMO. My only caveat is not having a extrapolated discovery and reserve growth developed in time for these models.

This is an excellent article as usual from 'Heading Out'. But I am finding some of the production numbers for Angola very difficult to understand.

From the article:

The numbers above would seem to indicate that either Angola produces massive amounts of natural gas and NGL (and whatever else is implied by 'mbd vs. mbdoe') OR "some technical problems with with water injection" have caused a recent drop in Angola oil production of over 2 mbd!

This becomes even harder to reconcile with the next statement about Angola exporting 1.7 mbd of oil, while the next chart (from EIA) shows domestic oil consumption in Angola of no more than roughly 0.1 mbd. The same chart would seem to say that the 3.8 mbdoe rate for Angola in 2010 (from BP) was a huge increase over the rate shown on the EIA chart in 2009, at least double.

Am I just missing something here?

don't feel alone, that's what hit me too.

Americans use 5-10x more oil per capita than Asia. Asia has 10x more people.

Are electric cars the answer? Is more oil the answer?

Bottom line. If every Chinese family buys a car, American families will not be able to afford a car. Oil dependency is a zero-sum game.

Footnote: Check out the form of government for the countries on the left column.

> are electric cars the answer?

What's the question?

If it's energy, the answer is no! We need 10X improvement in energy per unit of mobility, not 1.7X (or whatever).

If it's materials, the answer is no! EVs are heavier than cars. We need to learn how to do more with less.

If it's safety, the answer is no! EVs are no safer than cars. Cars kill a million people a year.

If its congestion, the answer is no! EVs are necessarily tanks (safety after all). Moving a ton to move a person is an engineering travesty.

Hmm, sounds like a good time in history to rethink our options.

> Is more oil the answer?

What is the question?

If it's equity, haves vs have-nots, the answer is no! We've squandered oil at the expense of world peace.

If it's our grandchildren's interests, the answer is no! We would serve them better by leaving some in the ground.

If it's pollution, the answer is no! There are cleaner ways of getting around.

If it's economics, the answer is no! There are far cheaper ways to do transportation (not to mention chemical uses of oil).

Hmmm, sounds like a good time to take a deep breath and reconsider what we are doing to our planet, to learn how to replace oil with ingenuity.

It's time to join the solarevolution!