The North American Red Queen: Our Natural Gas Treadmill

Posted by nate hagens on November 9, 2006 - 12:12pm

North American natural gas producers are likely in Georges shoes...

"Well, in our country," said Alice, still panting a little, "you'd generally get to somewhere else -- if you run very fast for a long time, as we've been doing."

"A slow sort of country!" said the Red Queen. "Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!" Lewis Carroll - "Through the Looking Glass", 1865

As was disussed here, the North American natural gas situation has a) been a story of two separate markets - flat to declining supply and flat to declining demand and b) the volatility in the market is giving policymakers the wrong long term price signals for this valuable commodity. (For basics on natural gas, both conventional and unconventional, search writings on theoildrum.com by both Heading Out, and Dave Cohen)

Here, I update the supply side of North American NG with information I learned at last weeks ASPO conference. This post is based largely on the excellent and thorough presentation given by Dave Hughes from Natural Resources Canada (NRCan). His entire presentations (which I encourage everyone to read), along with the other ASPO presenters, can be found HERE.

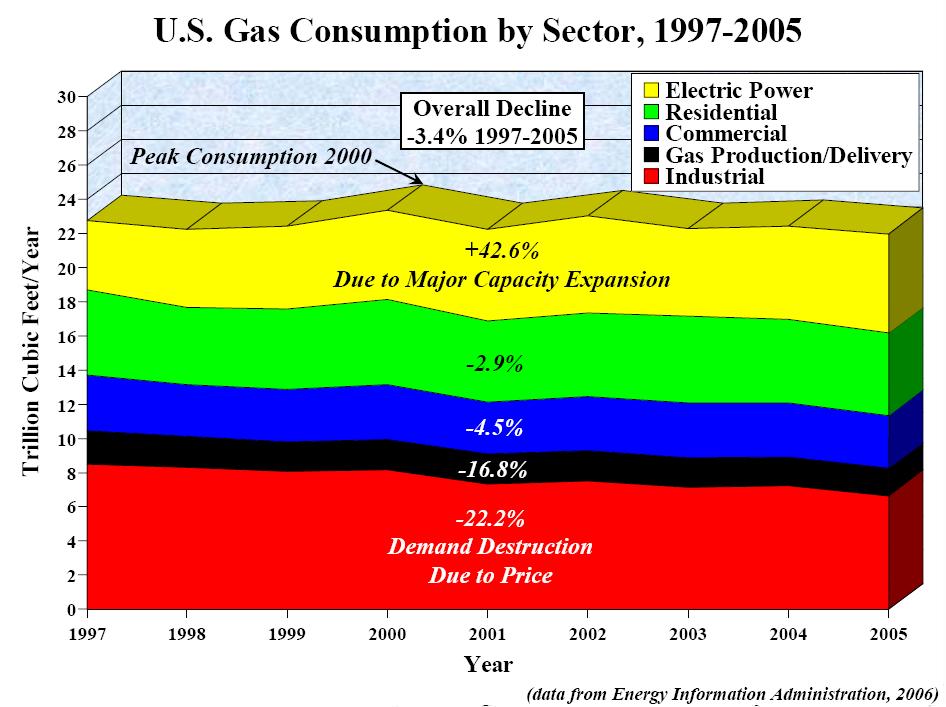

We need gas to heat our homes, make plastic, make nitrogen for fertilizer, make diapers, produce electricity, etc. Second only to oil, natural gas has many uses vital to our modern way of life. With the glaring exception of electricity due to large capacity buildout when everyone expected cheap gas of the 1990s to last, NG consumption has been declining domestically:

United States Natural Gas Consumption (Source David Hughes ASPO Presentation)

As can be seen, total NG consumption in the United States has been relatively flat over past decade. The demand side of the equation (almost as important as supply) is a story in itself and will be addressed in a subsequent post. With respect to supply, the good plentiful stuff has been found, pumped and used on our continent. The US peaked in production in 1973 with another peak in 2001. Canada appears to have peaked in 2002 and is currently piping 51% of her gas to the United States. Though there remains a large amount of natural gas reserves worldwide (though data is unreliable), it is difficult and expensive to transport. ( Dave Cohen will be writing on the LNG side of Mr Hughes presentation soon.) As the graphic below indicates, in the past 25 years, Canada, United States and Mexico have gone from having 12% of world reserves to 4% and we have 10 years of reserves at current production rates.

{kind=link}

{kind=link}

World Natural Gas Reserves (Source David Hughes ASPO Presentation)

We are drilling more, finding less, what we do find depletes faster and has fewer cubic feet. The below graph sums up much of the Canadian NG situation.

The Canadian Treadmill (Source David Hughes ASPO Presentation)

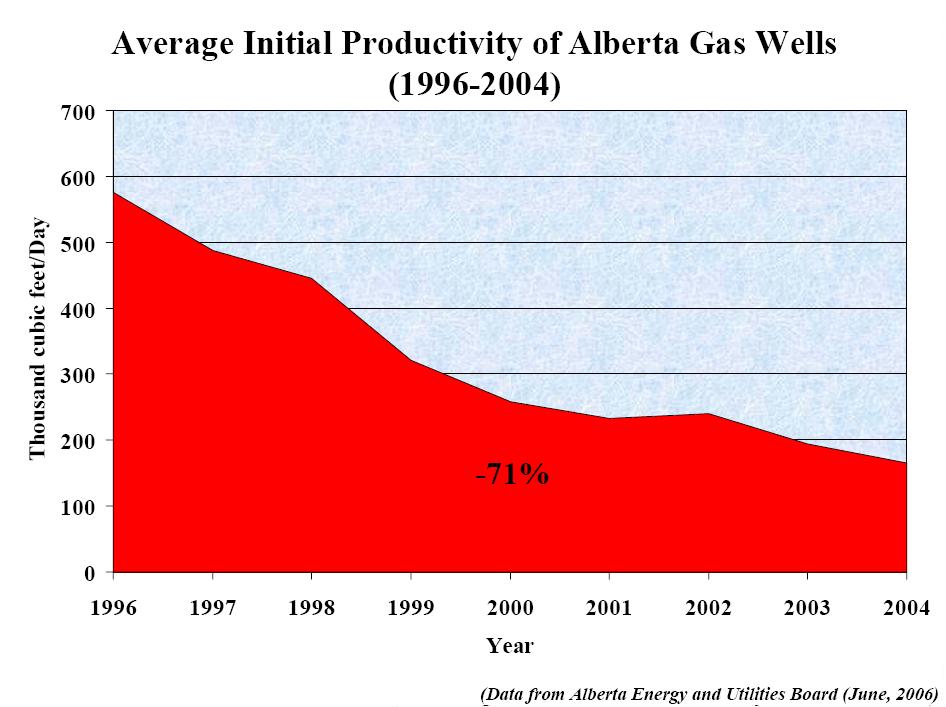

Not only does Canada use more rigs, but each new pinprick in the earth is producing less of the commodity and at slower rates. The province of Alberta has about 3/4 of the gas reserves of Canada. The trend of the below graph is obvious:

Alberta Gas Productivity (Source David Hughes ASPO Presentation)

With Alberta also increasingly using NG to turn bitumen into oil (or gold into lead as Hughes repeated), how does the priority chain stack up for the remaining NG reserves? Other provinces?, more tar sands?, send it to USA?, heat Albertians (I think thats a word) homes? Not talked about much even in circles that have connected the dots of energy supply problems, are the local and regional alliances that may or may not fall along traditional borders. Another post for another day...

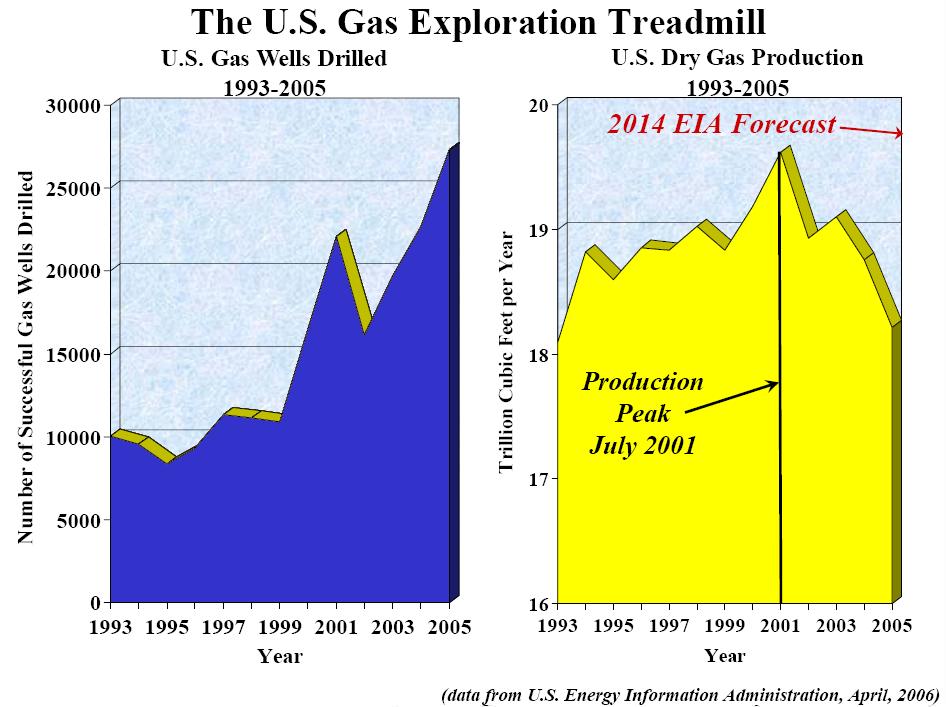

Lest we forget, there is another treadmill south of the border. Here is US production:

United States Treadmill (Source David Hughes ASPO Presentation)

By 'treadmill', I mean we are drilling more and more just to stay in place. As geology turns up the speed of the treadmill, we may not be able to keep up at prices consumers can afford. Indeed, Mr. Hughes mentioned (and this point was echoed by Matt Simmons)that if we stopped drilling today, we would produce 30% less gas next year, and 30% less the following year, etc. In other words, without an athlete running on that treadmill, we'd be down to less than 25% of our current production in just 4 years. And this is the AVERAGE depletion rate - new wells drilled today are depleting at up to 60% or higher. (In Canada first year decline rates are as high as 39% but tend to become less with successive years (ie production follows a parabolic decline). The overall decline rate in Canada is now about 20%).

And the new fad (old technology) of horizontal drilling used by Devon Energy and others, in effect gets gas out of the ground even quicker without meaningfully increasing the total EUR. (Its like the industry found a bigger straw, and since society is thirsty, the default strategy is to get the gas to market as soon as possible. This is neo-classical economic behavior at its best, but as evidenced by Chesapeakes announcement last month to shut in production due to low commodity prices, has its lower boundaries).

The flattening of production is occurring with an overall increase in rig count, and the vast majority of rigs being used to drill for gas. Increasingly, rigs are moving out of the Gulf of Mexico (GOM).

{kind=link}

Cameron Gingrich, lead project analyst for Ziff Energy, a Calgary-based consultancy, says "The Gulf's gas will fall from 25% of the total U.S. supply in 2000 to 8% in 2014, as total offshore output will drop from 13.9 to 5.8 billion cubic feet a day.

This has additional 'Red Queen" implications. The gas productivity differs in Gulf of Mexico vs onshore. Equity firm, Johnson Rice, specializing in E&P companies, recently noted that the 65 rigs recently leaving the GOM (most for overseas), translates into 500-650 land rigs needed. Lest we forget that our other favorite fossil fuel is also desired, oil drilling is a source of demand for incremental rigs 330-340 rigs are being used for oil, up from 220 a year ago (Source - Johnson Rice)

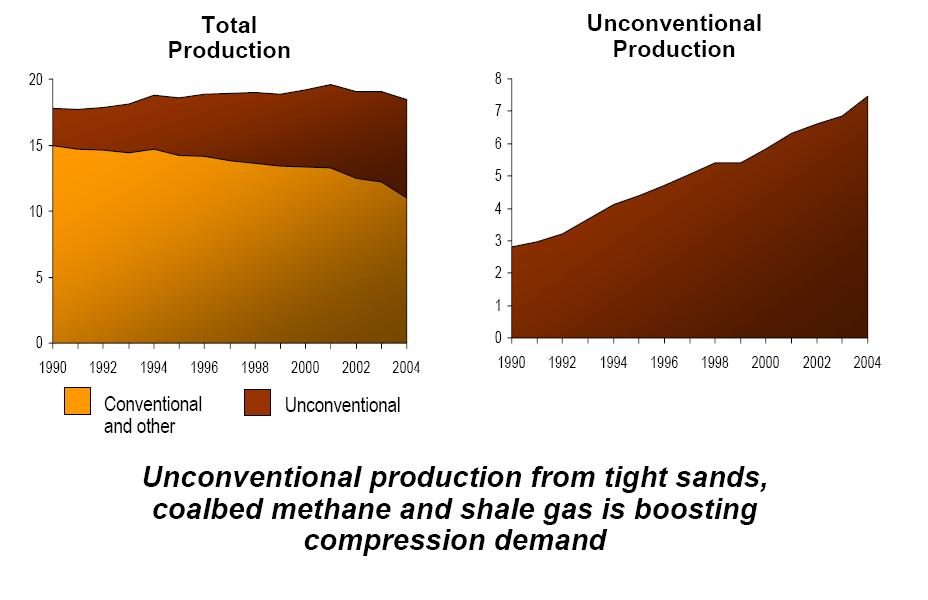

It's important to note that in the above graphic that the Energy Information Agency is optimistic that by 2014, despite the increase in rig count, faster depletion and smaller wells, we will make new highs in domestic production due to increases in unconventional sources, like coalbed methane (called coalbed gas in Canada) and shale gas. The below graph is data from the EIA on a UCO presentation:

United States Conventional vs Unconventional NG Production - (Source UCO Corporate Presentation)

I recently spent 3 months in British Columbia. One phenomenon I witnessed, and I expect more and more in the US, was vitriolic public reaction to proposed CBM development. I attended a rally in Smithers, BC, where residents were opposing a proposed CBM project in Telkwa, BC. 20%+ of the local adult population showed up to listen (heckle?) to a panel of government and energy officials explaining the merits of CBM for the community. The residents were concerned about the water quality of the Bulkley River (shown here with my dog Quinn), rightly so as it is their lifeblood and one of the best steelhead fisheries on earth. What was not discussed at the rally/forum was that without natural gas, how will people heat their homes in a town that has winter air inversion issues? (i.e. everyone using wood, would be bad)

{kind=link}

This type of public opposition is likely to intensify as we move from the easy, less obtrusive oil and gas locations domestically to more obscure, less quality ones in more remote/pristine places involving different land and water implications.. Unfortunately, our energy demands have laid the groundwork for an immense arms race between energy and the environment. Each time people raise their perceived value of ecosystems and nature, energy prices will be ratcheting up again. Tough choices are going to have to be made.

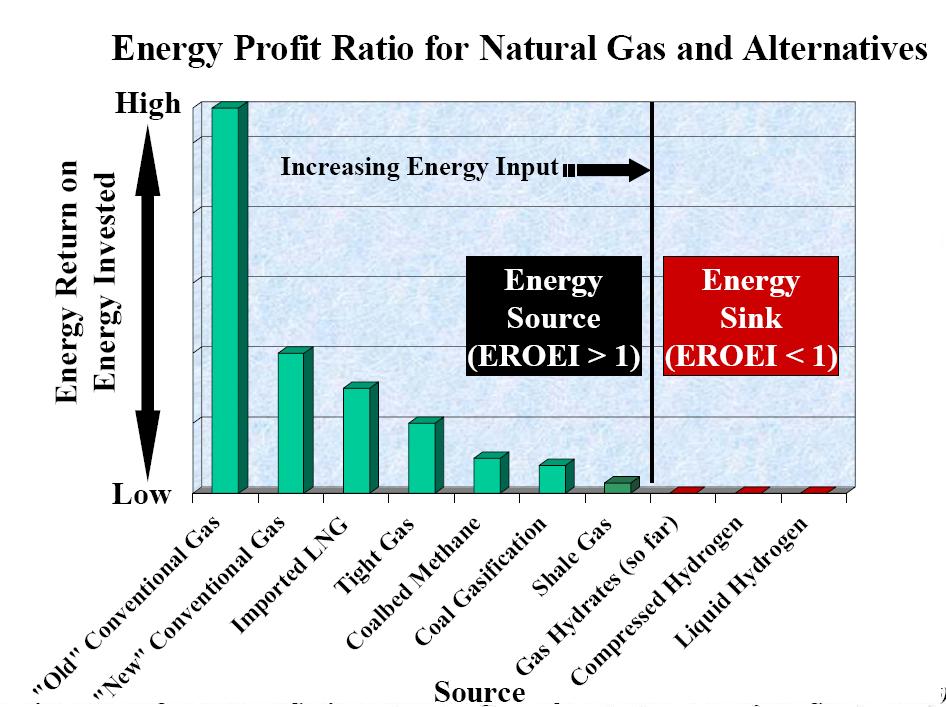

Energy Profit Ratio for gas sources (Source David Hughes ASPO Presentation)

In many senses, the story Ive presented so far can be explained by the above graph. We have used the 'best, first' for natural gas (and oil). The harder stuff takes much more energy (and dollars, and environmental externalites, and labor, and time, etc). A previous TOD article on net energy, or how much energy is left for society after the energy sector uses what it needs, can be found here.

CBM wells in the US with water production generally produce water for the first couple of years then gas with a lower decline rate. In Canada, however, most commercial CBM production comes from "dry" wells with higher decline rates - more like shallow conventional gas wells. (Source - D. Hughes). There is a large energy (and $) expenditure to get to the point where you are actually producing gas.

Dave Hughes Summary Points for NA Natural Gas(Source David Hughes ASPO Presentation)

Mr. Hughes pointed out that the amount of reserves that are energetically recoverable for the non-conventional sources are much less than the total reserves in government forecasts. The total area in each of the above triangles represents the gross resource while the black area represents the net. While government and industry are accustomed to quoting gross reserves, society cares about net energy. (well they don't but they should.) The Red Queen analogy is basically a net energy argument in a Tainter sense - the more resources we throw at extracting resources, the less the rest of the economy can grow.

Technology will attempt to buttress the decline in the net energy and quality of fossil energy sources. However, in many cases this 'benefit' may end up being a Faustian bargain. As horizontal drilling techniques speed up the flow of gas in order to stay on the treadmill, they change the ultimate depletion profile of the resource,(and I now include oil in the discussion). The technology that Devon Energy uses for gas wells in Texas or SaudiAramco uses for maintaining pressure on Ghawar, is getting us extra production today but at a cost of borrowing from the right hand of a typically bell shaped distribution curve.

By taking the energy from the ground we are borrowing from the future to begin with ( a loan from mother earth?). By using advanced techniques to get it out faster, we are adding 'leverage' to the equation, in a situation when our financial system has already maxing out on credit. In my experience as an investment manager, leverage always ends badly.

SUMMARY

I encourage everyone to read the online pdf of Mr Hughes ASPO presentation- there is much more valuable information than I could present here.

Here are Mr Hughes summary points:

Dave Hughes Summary Points for NA Natural Gas(Source David Hughes ASPO Presentation)

Later in the conference, Matthew Simmons equally interesting and sobering presentation also concluded on the topic of natural gas:

Matthew Simmons closing slide from ASPO/Boston(Source ASPO Presentation)

THE BOTTOM LINE

Natural gas is very important. It is also not easily transportable other than over land. Conventional natural gas in North America is past its peak. It is well past the peak of the easy to get at, environmentally (relatively) friendly, and energetically highly profitable point. To get more, we need more rigs, more holes, more places to drill, and more by unconventional means such as shale gas. Alternatively, we could buttress our treadmill with Liquefied Natural Gas imported from Qatar, Russia, Iran (the vast majority of reserves), or elsewhere - this may or may not come to pass, but will probably be written on extensively at theoildrum.com.

We have taken the low hanging natural gas apples from the tree and now have to climb the tree. Soon we will require ladders. Eventually large ladders and parachutes. To get that last apple we might need a helicopter and commandos, who eat more than one apple a day in any case. We should take advantage of these mid-tree apples and use them to our best advantage, while trying to replace as many apples in our diet with pears (wind), peaches (biomass), oranges (solar), or a wafer thin dinner mint (conservation).

If the treadmill really speeds up, at least we have Astro to keep us warm.

Contact

- Content: editors at theoildrum dot com

- Tech support: support at theoildrum dot com

License

This work is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License.

I've also been using the Red Queen analogy lately in so far as it accurately describes not only the natural gas situation in North America but also global oil production.

At some point, however, there are diminishing returns on this process based on thermodynamic, genetic, and physical limits. For example, race horses haven't gotten any faster in a long time.

Devon's horizontal well program is primarily in the Barnett shale. When George Mitchell figured this booger out, shale gas was generally uneconomic as well as the gas from coal bed methane. Therefore, horizonatal wells in non-conventional gas are recovering gas that would otherwise not be produced, not increasing the depletion rate of existing fields.

Second, the increase in land drilling depths over the last 25 years has in effect doubled the amount of gas-prone sediments to be explored. Most gas is found at deeper depths than oil in conventional reservoirs, and many promising trends have not been explored sufficently at depth to rule out their gas potential. How many coastward salt domes have been explored for deep Yegua and Wilcox gas?Woodbine/ Also, and I'm not a good enough earth scientist to answer this one, does the sub-salt structural trend exist on onshore domes? Is anybody running 3D seismic on these structures? Nobody has really stepped into the Major's shoes in onshore exploration and most of the independents that are left are focused on "sure things" like Cotton Valley/Bossier and unconventional gas.

I have no doubt that future gas will be expensive in the US, but I'm sure not willing to give up.

Bob Ebersole, aka oilmanbob

I've thought for a long time that ExxonMobil is a bigger threat to the US oil and gas industry than is Nancy Pelosi--because ExxonMobil is out there promising "Trillions of Barrels" of remaining oil reserves, plus vast natural gas reserves. When those alleged "reserves" don't show up as production, the public--and Congress--are going to be in a very ugly and vindictive mood.

For the producer, the important ratio is that between production cost and sale price (profit). Declining EROEI, barring significant and cheap technological advance, implies rising cost of production. Rising energy production costs do not lead to more disposable income among consumers (individuals, institutions, non-energy sector industry), but to less (in the aggregate) as economic activity shifts to energy production.

At the same time, government facing the loss of revenue from individuals and non-energy sector industry negatively affected by rising energy costs, will be looking to make up the difference. Pelosi's position to which you referred yesterday is just one expression of this inevitable tendency.

NATE: Thanks for the post and the links. Just a small comment about residents of the Bulkley Valley. They don't need natural gas for heating, etc., but can use wood. The key is in the technology. Hi-efficiency pellet and chip furnaces produce very few emissions. The last time I was up in that country, in the 1970's, the bee-hive burner was common and air pollution often horrible. I believe that the bee-hive burner is only an industrial relic today. In fact, I suspect that if every houshold, business etc changed from gas to bio-mass air pollution levels could still be reduced, as long as through incentive or regulation the wood burners (fireplaces, inefficient stoves) currently in use were shutdown.

Currently, wood pellets are shipped from the Ridley Terminal in Prince Rupert by the container load.

There is also of course geo-exchange.

By the way - the vast majority of pellets being made in BC (and now they have enormous capacity due to pine beetle killing of pine trees), goes to europe. I dont think many residents there use pellets - though it would seem to make sense to do so.

The announcement focussed on drilling in particular.

Cited reason - "Inefficiency has crept into the business as a result of having so much activity ramp up in such a short period of time."

But also:

Perhaps they'd rather hang on to some of those targets and deliver more of the stuff later, in a declining resource envrionment.

Or maybe they are just too busy building their new billion dollar office tower in Calgary ;-O

How has their projected production matched up with their results? These guys are better promoters than I am, but investors generally get discouraged when the production and prices are not up to snuff.

Could this have anything to do with slowing of drilling activity?

They are one of the largest land holders (last I checked, which was about a year ago, the largest land holders in oil sands) plus made some smart moves in unconventional gas in years gone by. They were considering converting to an income trust this year (now put on hold by the Canadian govt decisions announced Oct 31st).

Seems to support "we've got the resource, why race to pump it out when costs are high, when we can wait, and still produce huge profits".

I am optomistic that we can use natural gas for a lot longer than the ten year reserve life that seems to be implied by the article. I don't think its the 100 years that the Cornucopians we suggesting a while back, but it can hopefully ease the transition to a post fossil fuel economy. Now I'm really sorry I couldn't make it to Boston, it was Parent's Day Weekend at Texas A&M Galveston where my son is a freshman, and I had some other family obligations.

Could you point me out some reading on the sub-salt trend? I'm pretty vague, but how is it substantially different from salt dome overhangs?

Bob, I didnt imply we have 10 years left of gas usage, but 10 years left of reserves. This can increase or decrease over time as this graph shows. The implication is that continuing to keep our reserves at '10 years', given the treadmill, will be difficult. 100 years no way.

I have another question: What about plain old economic return on investment? How long can we still drill $2-$5 million dollar wells for 300 mcfpd wells? Not very long at $6.50/mcf.

One of the problems that Chesapeake has with its program is paying $10,000 per acre for DFW Airport. They have borrowed beaucoup money, and thats why I think their announcement of a 6% voluntary production cut is BS. I believe it was predicateds by their gas purchasers, not prudence. Gas contracts don't work that way, the purchasers tell a producer what they will buy, not the other way around.

As energy prices increase, the same phenomenon will be seen in many other commodity markets. As diesel and fertilizer goes up, farmers will not make money unless corn is higher. If corn is low, they will plant less (or none, but then maybe that is bad example - most are kind of stuck and have to plant SOMETHING).

To me, the smoothing out of nat gas supply and demand, given the above analysis, will borrow from general economic growth no matter how you slice it.

"...deliverability of these existing CBM connections is expected to be 10.4 million m3/d (0.37 Bcf/d) by the end of 2006, 8.9 million m3/d (0.32 Bcf/d) by the end of 2007, and 7.7 million m3/d (0.27 Bcf/d) by the end of 2008."

National Energy Board 2006-08

"As conventional gas resources deplete, CBM is projected to become an important component: it will supply about 12 percent (620 Bcf) of total natural gas production in 2020. If CBM is not developed at this rate, there will be implications for Canadian exports."

Canada's Energy Outlook 2006

Now that we have a new government in power, one must ask, "Will anything change?" Of course not. The emphasis has gone from lining the pockets of the oil companies to making more energy heroin available to the consumer at a cheaper price. When the heroin runs out, the addicts will go into withdrawal. Hello insanity.

As you may have noticed, the price of oil is on the move -- up. Now that the Saudi Arabian effort to lower prices by damaging their oil fields in order to prop up their pal, George, has failed, we will see another spike. Just in time for the heating season. Hooray!

If you can afford it, I would still advise anyone who wants to see some of the cultural treasures in Europe to go now.

Also, if you use Natural Gas to heat and cook, look into ways you personally can conserve. Some of these include:

- Install an automatic thermostat, where you set times for the heat to automatically go on and off.

- Insulate your house. Install weather stripping.

- Get rid of your hot water tank and switch to an instant hot water heater, or go solar.

- Upgrade to a more efficient furnace.

In my town there are rebates and tax credits from the utilities as well as the federal government to make these upgrades more affordable. In most cases they will pay for themselves at current gas rates in 3-5 years.Lastly, I would love to see the way Natural Gas is billed changed. Currently, the first 150 therms I use in the winter cost more then the therms after that! That's crazy, and it does not promote conservation.

Garth

I got a great oven, at a great price, from AMPOD's store.

Fares will be so many weeks on the ROW maintenance gang for those without the funds.

For the deep doomers, running the essential railroads may be the key to preserving some social order.

Best Hopes,

Alan

What crash?!?!

From two charts in the article:

World NG reserves have INCREASED for the last 20 years.

Meanwhile Natural Gas consumption in the US has decreased 4%, even with the massive increases in Electrical generation via Natural Gas.

I realize NG is not as transportable as Oil, and that it is a finite resource, but as a previous poster pointed out deep drilling should be able to unlock more reserves.

If we can curtail electrical generation via Natural Gas we should be able to carry on for quite a few more years. It does reiterate the need though for Nuclear, Wind, and Hydro.

For petroleum however, the global web of just-in-time goods deliveries doesnt have this same demand destruction option without seriously hurting growth.

I think we will see decline in gas supply, AND decline in gas consumption until we are near the bare bone minimum, then prices find a new long term floor at least double where they are now.

I'm not sure about this. Most of our decline in NG consumption over the last decades was probably driven by off shoring of base manufacturing. We may be much close to inelastic gas consumption than we think.

Also the additional gas needs for refining tar sands and heavy sour crude are not insignificant so as crude grades decrease gas usage goes up for refineries.

The only place I see gas use decreasing significantly is by switching to coal fired electric plants but I think our ability to deliver more coal via rail is close to its limit.

I could be wrong of course but generally it seems predictions of the elasticity of demand seem to be incorrect. Its sort of like the tragedy of the commons basically ascertain consumers drop out others that can afford the resource expand usage to keep demand almost constant if not increasing. For example industries that can pass on rising gas prices as surcharges can easily continue to operate. To date the only demand destruction that seems verifiable is in third world countries.

The real important ones IMO are the wells drilled v reserves depletion - it won't be long before production turns down too.

The other real interesting chart is the declining initial productivity of wells.

You are on a treadmill that is running faster and you are getting more and more tired - eventually you fall off the back and break a leg.

I posted a comment a week or so back about Baker Hughes Inteq share price getting clobbered when they announced their N American Nat Gas drilling would be down - this in response to your nat gas glut - I commented some where that your markets are going meta stable. Unlike in the past, with "big wells" that could be chocked back and turned on as needs require, wells are now just producing what we call "a wee fart of gas". So when stocks start to run down, you will need a drilling sprint to try to catch up - I feel so much better living in the UK where we have ample supplies comming from Russia.

Also like the EROEI chart which I am just away to send to our local "energy journalists' who don't know their arse from their elbow. I had a letter published in the local press today - copy in staff section if you have'nt seen it.

So how's the weather - your economy depends on it. Its turned chilly in Aberdeen so I've decided I don't beleive in Global warming any more.

Cry Wolf, I knew this, so put the pictures in expressly for you (well, you and my brother)

Natural Gas[p]! A conversation with an Industry Insider

He called around to various oil companies, trying to get someone to talk to him about the natural gas situation. Most refused, but he found one executive who agreed to an interview, as long as his name and company were not revealed.

This unnamed executive indicated that Matthew Simmons is likely correct on the U.S. natural gas situation.

But perhaps most striking was that the energy industry did not see "peak natural gas" coming.

The energy industry did not see peak oil USA coming. They were blindsided by peak natural gas USA. This despite having access to the best data and the best technology money can buy. So why should we believe them about the world peak?

Will it run out earlier? Later?

Another example of diminishing returns for EROI as described for oil in a prior thread.

Yep!

Natural gas is mainly consumed by industrial activities:

Natural Gas Flow, 2005 (Trillion Cubic Feet)

Natural gas is mainly consumed by transportation:

Don't forget Libelle's post (TOD:Canada) Fuel Prices As We Go over the Top...?

We have already come very close to running out of natural gas. (The winter of 2004, I think. By the end of March, we were one short cold snap from equilibrium pressure in the pipeline from the Midwest.)

There have been power emergencies declared in winter around here. Usually, they happen in the summer, but we have had a couple in the winter in recent years.

Some large customers (big companies, government offices, etc.) get a break in pricing, in exchange for agreeing to shut down during power emergencies. The local politicians also get on the air and ask people to conserve. If that's not enough, the rolling blackouts commence.

The gas storage according to http://americanoilman.homestead.com/GasStorage.html was:

3/16/2001 799

3/15/2002 1936

3/14/2003 654

3/12/2004 1097

3/11/2005 1379

3/10/2006 1832

What made 2004 just about cause the problems and not 2001 or 2003? Or did 2001 and 2003 have problems also?

Thanks,

Rick

I think it was just the vagaries of weather. Cold winter = lots of natural gas use. Heck, hot summer = lots of natural gas use.

One of these years, we're going to have a hot summer followed by a cold winter. Then the TSHTF.

1)The northeast predominantly uses heating oil as opposed to the rest of country uses nat gas in winter

2)something I might write on, is a certain (not small) amount of gas in the pipeline needed to keep the pressure up enough to be able to deliver the rest of it. In other words, we cant 'use' all of our storage. Im not sure what that number is but if memory serves its around 800 bcf. Anyone?

Interestingly, the EIA wrote a paper on gas storage in 1997, with plans to increase it, etc. but the storage in US has not increased since.

Not true. The northeast consumes most of the heating oil used in the U.S., but it doesn't follow that most northeastern homes use heating oil. Indeed, only 1/3 of homes in the northeast heat with oil. 47% use natural gas.

roughly, each US winter

5 Quads Nat Gas

1 Quad Heating oil

1 Quad space heating

some amount of wood that is small compared to those 3.

This is just a guess, but my feeling in rural (and even suburban) anywheresville, NE USA, is that there is a lot of wood burning going on. Perhaps mostly for demonstration reasons (nice wood fire in the living room) but it could be significant (and relatively hard to measure, given that a lot of the wood will be either bought informally (no sales tax receipts) or burned from own-sources).

http://www.localenergy.org/research_bioenergy.htm

I think that Hothgor's comment above on closing rooms could be an cynical attempt to build credibility, as might be the case with some other of his comments, in the hope that that credibility will carry itself to other interventions. But in itself, his proposal is not an unworthy idea, nor does it insult anyone, or the intelligence of all.

I believe it is better to respond to Hothgor in measure of the content of his posting. Mostly I believe it is better to ignore him, though obviously some comments require a response.

While I learned nothing in the way of fact from the 'debate' between Hothgor and Westexas, I found that it did serve as a review and that it did improve my understanding of methodology.

And mostly, I learned that Westexas is a gentleman as well as a perceptive analyst.

IIRC, Hothgor used 2 graphs, one of which was mine (showing YTD imports [crude + products] 2005 v 2006) to be nearly identical. He didn't misrepresent my graphs (although an attribution would be nice) but I wish he would stop using cusswords - not the way to win friends and influence people.

Also unanswered from yesterday, Oilmanbob, do you dispute Hothgor's claim that Colin Campbell has repeatedly revised upwards his peak date and URR numbers? I didn't think any one disputed that.

A week ago your comment might have been worth something. Hothgar is just too heavily backed this week. He's been given this backing because we want to see what he can do. He can wake-up and decide to take the day off, or he can run full-out. It's up to him.

I can assure you that there are other full-on assaults in the works. Maybe some of us just need diversions. Maybe not. Surprise is key.

Long Live the Hothmeister!

Its all coming, pity the future is so late getting here.

My 'inside man' on power tells me that you have to keep spinning the turbines, if you are using coal as peaking power, even when you are not drawing power, to avoid the wear and tear of cooling down and heating up the steam system. (American utility practice)

Ontario Hydro would use coal as peaking power, and actually power up the turbines (which the Americans thought mad).

So roughly the merit order is:

- nuclear

- hydro (depending on flood control regime in place)

- coal (typical mid merit)

- gas (CCGT-- the combined cycle bit also doesn't like being heated up and cooled down quickly)

- oil or gas fired turbine (almost instantaneous readiness)

- (panic ;-)

A related complexity (which I haven't entirely sorted out in my own head) is that the CCGTs in the 90s were all built with project-specific finance debt. So as long as the spark spread (the cash gap between fuel price and electricity pool price) is positive, the CCGT will bid in to the pool, to generate cash, to create cash flow to service the debt.This would imply gas running in mid merit. Which I think it does in the UK, but I don't know about the US markets (not all of which are deregulated).

At first it seems that you might (at least in theory), but if you add the necessity for water management for other purposes, it starts to look next to impossible.

Pumped storage is another means of balancing wind and storing power for a week or three. Excess late night wind used for peaking a week or so later.

Best Hopes,

Alan

some interesting thoughts on pumped storage, using disused mines.

The report is pretty conservative: I think the things it leaves unsaid are:

- Ontario's 14,000MW of nuclear capacity will have to be replaced (with nuclear). That decision will have to come soon (probably c. 2010)-- which the report does point out (to have new plants operating 2018-2020).

- it doesn't assume any coal and carbon capture by 2020, but the implication is after that, there will have to be same

- there needs to be an integrated power strategy with Manitoba and Quebec, but between Indian land claims, environmental concerns (which ignore the current tradeoff, which is to import coal-generated electricity from Midwest power producers), transmission-line siting (in a Parliamentary system with geographic districts, you can lose crucial ridings (seats) by approving a new 512KV line), and pure politics (the Prairies hate Ontario, Quebec hates everyonel, everyone hates Quebec), it's hard to see this emerging

It's crazy to close Nanticoke (largest coal fired station in North America, with relatively advanced scrubbing technology) to buy coal-generated power from the Midwest. But that is policy, right now.Nothing is.

But if you have a poor snowfall (talking here in Canadian or alpine context) then you won't have the water reserves in summer.

Hydrology management becomes brutal: do you kill the fish in the river (by insufficient flow) or do you shut down vital industries? Destroy the livelihoods of local Indians, or blackouts in Toronto?

Much of northern Canada is actually effectively a cold desert. The growing season is so short, one doesn't notice.

But the rivers can dry up, and this is not impossible in a global warming scenario.

This is particularly a problem in Northern Alberta, home of the largest oil reserves (as tar sands) outside of Saudi Arabia. That oil production needs water, and there isn't a whole lot extra to spare (although I haven't sized it against likely oil sands related demand).

What do I disagree with? Well, it's the statement 'Risk of Peak Gas if far more worse than Peak Oil'. The partial disagreement isn't about how important gas is. It's just that when one fully understands Peak Oil, or rather understands Peak Oil the same way as I do if they indeed are 2 different types of understanding, the notion of Peak Oil already covers Peak Gas and pretty much everything energy related. Peak Oil in my book doesn't mean what it meant some years ago. It has transformed into a larger concept that now covers just about all energy related problems. Perhaps today, while feeling particularly arrogant, I would even put Global Warming under Peak Oil although at first glance it might not make much sense :)

However.. even though you probably classify me as a mental case even though you wouldn't want to actually say such a thing, I still want to say, again, that I love your work.

There is one aspect where I disagree. In the event of even higher oil prices, I read comments that American consumers would outbid poorer countries. I suppose such poor countries include India and China. But I do not agree to that. I believe in such an event, consumers in India and China would outbid Americans. Reason I am saying is this: these two economies are growing at about 8 and 10% respectively. And they are growing because there is a lot of investment that arises out of savings. India saves about 30% of it's GDP and China about 40%. And when oil prices rise considerably, these economies would slow down, no doubt, but they will still be able to buy oil by drawing from their savings. We all know Americans don't save. They not just don't save, the country runs huge debt and is probably bankrupt (thanks to it's pension policies). So, they simply would have to conserve. Infact, this is exactly what is already happening. China and India are consuming more and more oil every passing year. While we certainly are facing oil supply issues, these demand increases have certainly helped increase oil price. So, I would say China and India will outbid American consumers. Americans consume way too much oil and it will badly hit them.

Welcome! I agree in principle with your valid points. Unfortunately, in todays world, the 'ability to pay' is a spectrum that passes right through the zero point on the scale. Americans (private and govt) can just borrow more to pay for oil - using their steep discount rates to value the present over the future, intending to pay it back after they use the leverage in the oil to make something or feel good.

In theory you are right, because the behaviour I mention above cannot last. But we will pay for the oil, with credit or other means, I am sure.

Maybe you meant "intending to inflate it back in future"? I don't think anybody seriously believes that we intend to pay off our evergrowing and ever-accelarating debt, not at least at its initial real value.

- the big buyers of US treasury and mortgage-backed securities have been offshore central banks (chiefly Far Eastern).

They are doing this because if they sold the US dollars that are constantly piling up (due to the export surpluses of their countries especially China but also Japan, Korea, Taiwan etc.) then their currencies would appreciate.

But that would cause domestic economic (and eventually political) stress. China in particular has struck a bargain with its people: accept the role of the Communist Party and the restrictions on personal freedom and political expresion and we will make you rich. To make you rich, we will export.

Once they have these huge reserves of US dollars, they have to stick them somewhere safe, and liquid. No market is safer or more liquid than the US Treasury Bond market. They treat the mortgage backed debt of the GSEs (Fannie Mae, Freddie Mac, Ginnie Mae) as effectively US Treasury guaranteed debt, so they hold that as well.

- the flip side of this is of course that it is domestically convenient for the US. The Administration wanted tax cuts, regardless of the outcome on the government surplus, and for the economy to grow, especially post 9-11.

(the late 90s bubble was the stock market and dot com bubble and that drove consumption. The 2000s recovery has been about the housing market, and associated consumer debt, and has been far bigger. Robert Shiller (who called the first bubble accurately in 1998) has called it 'the biggest bubble in world history' (estimating the rise in US housing price valuations over historic norms))

The US kept the economy ticking over by running the largest housing boom recorded since the immediate post war years (when the veterans returned home, and were offered mortgages for the first time). The appreciation of US housing had a number of effects on US consumption, all of them positive. (the raw effect was a 2.0% increase in the proportion of GDP devoted to residential construction: from 4.5% at any previous peak, to 6.5% this time-- but there were multiplier effects throughout the economy, eg employment in housing related financial services companies like mortgage brokers).

- *what happens next?

1. the normal outcome when a country runs a large current account deficit (equivalent to shipping dollars overseas in return for goods and services imported) is to shrink that deficit by:

- a domestic recession (spend less, save more)

- depreciation of the currency

History says that current account deficits close-- they don't run at 7% of GDP forever, because if they did, eventually all the dollars in the world would be in the hands of foreigners. As Herbert Stein, Chief Economic Adviser to Richard Nixon put it 'what cannot go on forever, doesn't'.The Chinese now have a double reason to resist depreciation of the US dollar:

- loss of competitiveness to their own exports and potential for domestic recession

- portfolio loss on their huge USD holdings

So they will fight very hard to prevent a depreciation of the USD (which in practice means the Euro, as the third side to the triangle of the dollar-renimbi/yen-euro, will appreciate).It also means that the domestic recession could be worse than it would otherwise have to be.

2. the optimists think this won't happen. That the world has an almost infinite desire to hold US dollar assets, and therefore the current account deficit is not a reflection of the US living beyond its means, but simply the world economy's way of balancing itself.

The problem I have is that it is the flow not the stock which counts: ie at the margin a diminished preference to hold US dollars, will drive the US exchange rate and the US interest rate.

I don't think the US is about to be the next Argentina. Unlike Argentina in 2002, or Hungary now (appparently half of all mortgages in Hungary are Swiss Franc denominated), the US has borrowed in its own currency.

But interest rates can, and will go up. At some point, markets will get worried about the indifference of the Congress to soaring deficits, and the marginal holder of US treasury bonds will demand a higher return to buy more bonds.

At which point, interest rates will go up. The housing market will go down. And the US will be forced either to consume less, or export more.

If that transition happens fast, it's going to hurt. Switching Americans from working in housing finance and housebuilding, and other 'non tradable' sectors into working for tradable sectors (think Boeing, Caterpillar etc., and also import-substituting industries like eg office furniture or car assembly) doesn't happen overnight.

* note there was nothing like the demographic kick of previous housing booms in this one-- this one has been about people increasing the personal exposure to housing in their portfolios. In 1945, and again in the late 70s and then the mid 80s, you had big increases in the number of households. The US birth rate plunged in 1963 (so first house bought 1991) and didn't really begin recovering to the mid 70s (first house bought 2003), and it is still sharply lower than it was in the 1950s.

Of course this could have been prevented if a balanced fiscal and monetary policy has been persued from the very beginning, but it looks like it's getting to late for that. IMO there could be several outcomes from this situation, but none of them looks good. My bet would be on hopping inflation, interest rates rising but not that far, and slowly depreciating dollar all at the same time. The reason? It takes time for the credit holders to understand that they are losing the real value of their assets. This allows the FED to play the very old game of tricking the money holders by raising the rates a little bit lower than it would have to, or a little bit too late. All said and done in the end those 6 trillion or so now will look not that huge amount of money in 10 years. Just like the 3 trillion 10 years ago now look as pocket money.

Note that substantial Indian and Chinese savings are only possible as long as their economies are growing, and this is questionable too as world commerce declines with oil production and their exports suffer as a result.

I think it is hard to predict how the pain is going to be spread.

Along those lines, the head of the Peoples Bank of China quite clearly indicated this morning that China is going to diversify its foreign exchange holdings (in other words dump the dollar).

The dollar immediately dived against all currencies. I think that in spite of all efforts by the US and foreign national banks, the dollar is about to seriously devalue. It will not be a slow process. Currency exchange prices change incredibly fast, and I think the dollar value could easily drop in half in only one day.

No way. If that happened, I'd head for the bomb shelter. (Wait, I dont have a bomb shelter).

The G8 would never allow such a thing - even a 10% drop there would be massive intervention. If US$ dropped 50% in a day, the world financial system, which includes China, would be kaput.

My vote is steady and slow decline of dollar. Sharp decline would mean financial intervention and if that doesnt work, military intervention.

Remember, a declining dollar actually helps the trade balance of the US. The US is also Chinas biggest trading partner. If the US tanks, so does the Chinese economy. Do you really think the Chinese are going to commit economic suicide?

http://www.economist.com/business/displaystory.cfm?story_id=8049652

"Since 2001 the increase in emerging Asia's trade surplus has added less than one percentage point a year on average to the region's average growth rate of almost 7%. Contrary to the received view, the bulk of Asia's growth has been domestically driven. True, domestic demand (investment and consumption) has grown more slowly than GDP over the past year everywhere except in Malaysia (see chart 1). But in most cases the gap has been small, especially in China, India, Japan and Indonesia. ...

"It is true that exports account for 40% of China's GDP, but those exports have a large import component; only a quarter of the value of China's exports is added locally. The impact of a slowdown in export growth would therefore be partially offset by a slowdown in imports. China's GDP growth has come mainly from domestic demand, which has been growing by an annual 9% in recent years.

"The idea that China's growth is mainly export-led is not the only popular myth. Another, says Jonathan Anderson, an economist at UBS, is that China's consumer spending is feeble. Several recent reports highlight that according to official figures spending has fallen from 50% of nominal GDP in 1990 to 42% today. But this partly reflects an even stronger boom in capital spending. Real consumer spending has been growing at an average annual pace of 10% over the past decade--the fastest in the world and much faster than in America "

Globalization has caused the worlds economies to be intricately linked. If you have a disruption in one part of the link, and it will ripple out like waves in a lake to affect the rest of the world.

When you look at the fact that the US is roughly 1/5th of the total global economy, you can not possibly come to any kind of logical scenario in which the US can crash and the rest of the world continues on expanding indefinitely. When the US crashes, you lose the majority market for high tech items, a large part of the automobile manufacturing industry, and a sink for a large portion of the worlds disposable goods.

While it is true that Chinas economy is largely domestically driven, its being financed by US and EU companies. If the US tanks, their financing dries, up. If their financing dries up, their economy also tanks, causing EU companies to also pull out. At the same token, if China stops buying US bonds, our economy would tank, but as you can see that would hurt them just as much.

Simply put, China NEEDS Google, Wal-mart, GM and others to invest in their economy. Without it, it will cause social collapses that will eventually lead to the end of communist rule.

Who knows. I don't.

Actually, the case appears much the opposite. I don't disagree that China, from an economic growth perspective, benefits from U.S. investment, but US foreign direct investment in China is about 8% of total FDI in China.

But what would Wal-mart do if China decided that only Wal-marts competitors were worthy of cheap and disciplined Chinese labour? GM is losing money in North America, but making a profit in China. Was Google so NEEDed by the Chinese, that it could tell the regime to shove Chinese censorship?

In a capitalist system, kapital has to grow, which is why capitalists are lined up at the door to invest in new plant.

While the US is probably still the leading recipient in the world of foreign direct investment, interestingly little of it appears to be going into new productive capacity.

Takeovers yes, but takeover and expand in the U.S., no.

And previously Hothgor said, "When you look at the fact that the US is roughly 1/5th of the total global economy, you can not possibly come to any kind of logical scenario in which the US can crash and the rest of the world continues on expanding indefinitely."

Is 1/5th an accurate measure? Is the cause of the presumed US crash one, such as peak free energy, which would in itself affect all economies? But aside from these matters there another problem with your contention: When the US economy crashed during the Great Depression, it did not disappear. Even if you could assume that events might cascade until a quarter of US GDP disappeared, not a very likely scenario, the US economy would still be large. Farmers would still be looking for markets, as would be Hollywood and the arms manufacturers. And American consumers would still be in the market for goods no longer domestically produced. China would take a hit, but as the article in the Economist argues, it is well positioned to recover and carry on.

It may come as a great surprise to us in North America, but really we are of declining importance. This has been the trend for half a century and has never been more true. The silly neo-con adventure in Iraq has only accelerated this trend. And there is nothing to stop the decline in absolute and relative importance from continuing. American bravado or Stephen Harper's unfounded claims about a emerging Canadian energy superpower nothwithstanding.

Your assertion that the US economically has been a declining power for the past 50 years is bogus at best. If anything, the US economy became MORE important to the world following WWII as it was one of the only remaining industrial basins left. Back in the 90s, it was the US economy that kept the world going after the fall of the Soviet Union, and the economic impacts of the Japanese recession and Asian collapse in 1997.

Now I do agree that over the next 50 years, this is unlikely to be the case, you still can't write off the US economy in light of the rising stars such as China. Also, the economic projections of China's rise to power are grossly exaggerated. China is about to face a 4-2-1 problem in that 1 person will be supporting 6 others. It doesn't take an economics major to realize how much of a problem this will be, and it will be a far worse problem then anything the EU will experience.

In a way, this will limit their overall economic expansion in a way that global economist haven't accounted for...assuming we make it through the peak oil problem we're going to face :)

I don't know how you manage to draw this conclusion from what I wrote. Merely the fact that China's economy is more domestically driven than most people have taken it to be means that China is less dependent on exports to the US than we have thought and not as inextricably bound to ever growing exports to the US. I have no illusions that US-China trade will suddenly dry up, however, China likely can balance its trading and its investments to the detriment of the US economy while enhancing its own economic position, or, at the very least, not harming its own economic position. Altogether, this, along with all the other massive distortions in the US economy, bodes ill for the US.

Really? According to http://www.ustreas.gov/tic/mfh.txt not only are the Chinese still buying US Treasury Securities, but the latest month reported, August, showed the highest monthly total as far back as August 2005 (the extent of the data in the above link).

Do you really think those Brit bankers feel that we are such a great investment that they just have to buy our debt? The answer is no. That is monetization of debt in action

More than 1/3 of China's trade surplus went into Mortgage back securities. That was Chinas Dollar Diversification plan. China has been talking for years about getting away from the dollar and uncoupling the yuan from the dollar. Yet China has remained linked at the hip to the US dollar in order to keep its double digit economcy growth. Since China now has at least $1 Trillion in US Dollar reserves, it has a lot to lose by dumping the dollar.

I suspect that today's statements has a lot to do with the election, as the Democrats have been demanding that Tariffs, Trade limits and other restrictions be placed on China to prevent jobs from going overseas. China is attempted to preempt Congress from enacting trade restrictions by using its dollar reserves as a weapon.

Oh ho!

So, logically, they prefer a Republican congress and administration, historically less protectionist.

Makes one wonder, have they been propping up the US economy in order to help the Republicans? Are they more likely to pull the rug now?

China could care less which party is in power. All China is interested in doing is using US trade to expand its economy and prevent domestic deflation. The Global economy is hinded on trade with America. America is know as the market of last resort. If you can't find buyers elsewhere, dump it on america. "Americans will buy anything, even if they can't afford it."

Without American buying imported goods (on credit), there would a significant drop in global economic activity and it would probably trigger global deflation. Despite the fact the China is losing money every day by supporting the US dollar is irrevelent. China wants to keep its economy booming and China is well aware of what happened to Japan after Japan dumped the dollar in the mid 80's: 20+ years of deflation. China doesn't want that to happen anytime soon to them, and they will continue to support the dollar until they simply have no choice. If it wasn't for the presence of PO, China could probably continue to prop the dollar for another decade. Japan did it for last 15+ years even with a soft economy, China's economy is now much larger than Japan's and has really only been the leading supporter of the dollar for the past four of five years.

For more information about the US-China trade situation Google "Bretton Woods II"

If anything China might prefer the Democrats since they would less likely interfere with its role trading with Iran and other anti-western states, and hassling them over trying to lock in oil with long term contracts. If I recall, China provided substantial campaign funds to Gore during the 2000 election.

China has broken up in to warring states before. India has had its share of turbulence. Both of these scenarios could lead to a severe drop in demand in short order.

And, not just oil, but ng too; the 22% ng industrial demand destruction shown in this thread is on account of US fertilizer and petrochemical shutting down and the products imported from overseas on account of their access to cheaper ng feedstocks. This will continue, maybe faster than the declining supply, which is why I expect ng prices to be flat while oil rises, meaning that oily e&p's are, at the moment, better investments than gassy ones.

One advantage we have compared with many, in addition to producing maybe 1/3 of our oil usage and nearly all of the ng bit, is that US wastefulness means we could, if pressed by higher prices, consume less with relatively less pain... lighter, more fuel efficient cars and trucks, car pooling, more transport by rail and less by trucks, peal electrical pricing, etc.

US consumption of oil has increased by 20% in the last 20 years or so, or around 1% every year. Chinas consumption has increased by about 600% in the last 20 years. And as you stated, their consumption has increased by 20% since the rise of the oil prices.

When you look at consumption in that context, you can only come to the conclusion that China is bidding on the oil they need to expand their economy, not that they are outbidding the US.

Individuals, institutions (including local, regional and national governments) and companies buy oil.

What your numbers do show is that actors operating in China are in aggregate able to grow demand for oil at a higher rate than those operating in the US. The price of labour is a large part of the explanation of why this is so, though far from the only one.

For industry, it doesn't matter how many dollars there are in the US or for that matter in China; what matters is whether the oil can be consumed profitably.

At $50/barrel, industry in aggregate can expand in China. In the US, this doesn't appear to be the case.

The consumption of oil products is indeed subsidized by the Chinese state, which does lead to certain inefficiencies and arguably some benefits. Still, China pays the world price for imported oil. China has negative trade balances with many countries, including its petroleum suppliers. Domestic oil sold below market value bears an opportunity cost.

If anything the cost of inefficiencies caused by subsidized fuel consumption outweighs the benefits, thereby putting a burden on the Chinese economy not carried by the US or the UK.

Your observation is much like the comment often made in these discussions that Europeans pay twice as much or more for oil than do Americans thereby demonstrating that the US can expect minimal economic fallout if oil prices double.

In reality, the European economy pays the same world price for oil as the American economy. Individual consumers pay more for gasoline, diesel and so on, but the difference is tax money that is recirculated in the economy with postive effects for European welfare. The Chinese government circulates wealth via a subsidy on fuel. Perhaps this policy is linked to the problem of a wide disparity between rural and urban China. I don't know.

In North America we provide free roads as a means to circulate wealth, though public policy is slowly moving towards road pricing, and tolls have long existed in some places. But just watch the trucking industry scream every time a new toll is proposed.

As for china and their imports/exports, China exports value far more then their imports. As such, they can write off a fairly large portion of their oil expenditures, and subsidize the cost of oil for their populace.

1997 18,620 % change

1998 18,917 1.6

1999 19,519 3.2

2000 19,701 0.9

2001 19,649 -0.3

2002 19,761 0.6

2003 20,034 1.4

2004 20,731 3.5

2005 20,802 0.3

2006 -1.5

As you can see, the average annual US consumption increase from 1997 thru 2004, including the dot.com recession, was 1.6%/year, which is what the population 'wants' to accommodate 1%/year population growth plus avg gdp growth in a period of fairly stable prices. However, responding to high prices in 05/6, a period of low interst rates and good gdp growth, yoy increases declined sharply, with the first 7 months of this year dropping 5x as much as the recession year of 01. To put this differently, one might have expected the US to increase consumption by 640k/d in 05/06, but actually consumption has declined around 260k/d, the delta at around 900k/d, or 4.5% of US consumption. Ethanol may be playing a part, but so far produciton is only around 300k/d, so the price effect appears to be around 2/3, or 3%.

Meanwhile, during the same period this year, chinese imports are up 20%.

Replacing vehicles and building new infrastructure is not easy, especially when energy prices increase. That leaves car pooling and staying home. Unemployment may make the latter common.

Regarding importing food from US. Why would India do that? They will import LNG from Iran and Qatar, not food from US. I don't think US is competitive vis-a-vis India in agriculture.

And water in tankers? Can you give some numbers? What % of water is transmitted and distributed in tankers? And whatz your point? Even if some water distribution happens through tankers, it only shows that oil is too cheap. As prices go up, they will use pipelines. And it'z not as though crude oil would move from 60 to 600 within a year, to cut-off such water distribution to poor people.

There was a report a while back (think I read it here) about water tables dropping in India due to overuse. One of the examples in the article was a town who's wells had dried up The Indian government was forced to truck in water to keep the people alive.

I do believe this is what suyog is refering to (correct me if I'm wrom suyog).

I wish I could remember the article and link it for you. Perhaps another TODer with better memory could find it.

A quick googleing found this article about dropping water tables, but it is not the article I was trying to find.

As an aside I heard a realy facinating tidbit about water usage the other day on the radio (living on earth I believe). They said that there is a very large trade in water, in the form of wheat. It takes something like 1,000 tons of water to make 1 ton of wheat. Wheat exporters (USA, Canada, Australia) are really exporting their water to wheat importers. I guess its really similiar to the way China is exporting its energy in the form of raw good (steel etc).

This city will soon have desalination plant to augment it's water supplies. It is even contemplating a chip fab plant that requires a lot of water. If Indian government is willing to provide some sops, Intel would in all likelihood setup it's fab in Chennai.

I'll dig around and try try to find that article.

I've never been to India. Its high on my places to visit list. I do apreciate your input.

please keep posting.

Thanks

Rethin

And water supply through tankers: it is done to poorest of people in urban slums. It is not easy to provide piped water supply there and is probably not even legal. So, government supplies water to a nearby water tank from where these people carry water in their pots by themselevs or using bicycles.

India is a very poor and complex country. If you think you can understand this country by reading bbc or any other news sources sitting 10,000 miles away, then you are wrong. I suggest you come to India and live in urban and rural areas for a few years before you start making your comments.

Well that might be a little high of a bar.

Short of that most of our (westerners) sources are major news outlets.

I think that makes contributions like yours so valuable.

Honestly hearing that a thousand farmers commit suicide sounds pretty alarming to me, but you frame it in an Indian context. Fascitating.

Thanks

Our massive build in the 90's of combined cycle gas turbine merchant plants was quick and easy money for the developers but poor public policy. Fortunately, the capital investment in now obsolete CCGTs was low on an individual unit basis.

Eventually, most energy-savvy people are going to regret not building more nukes.

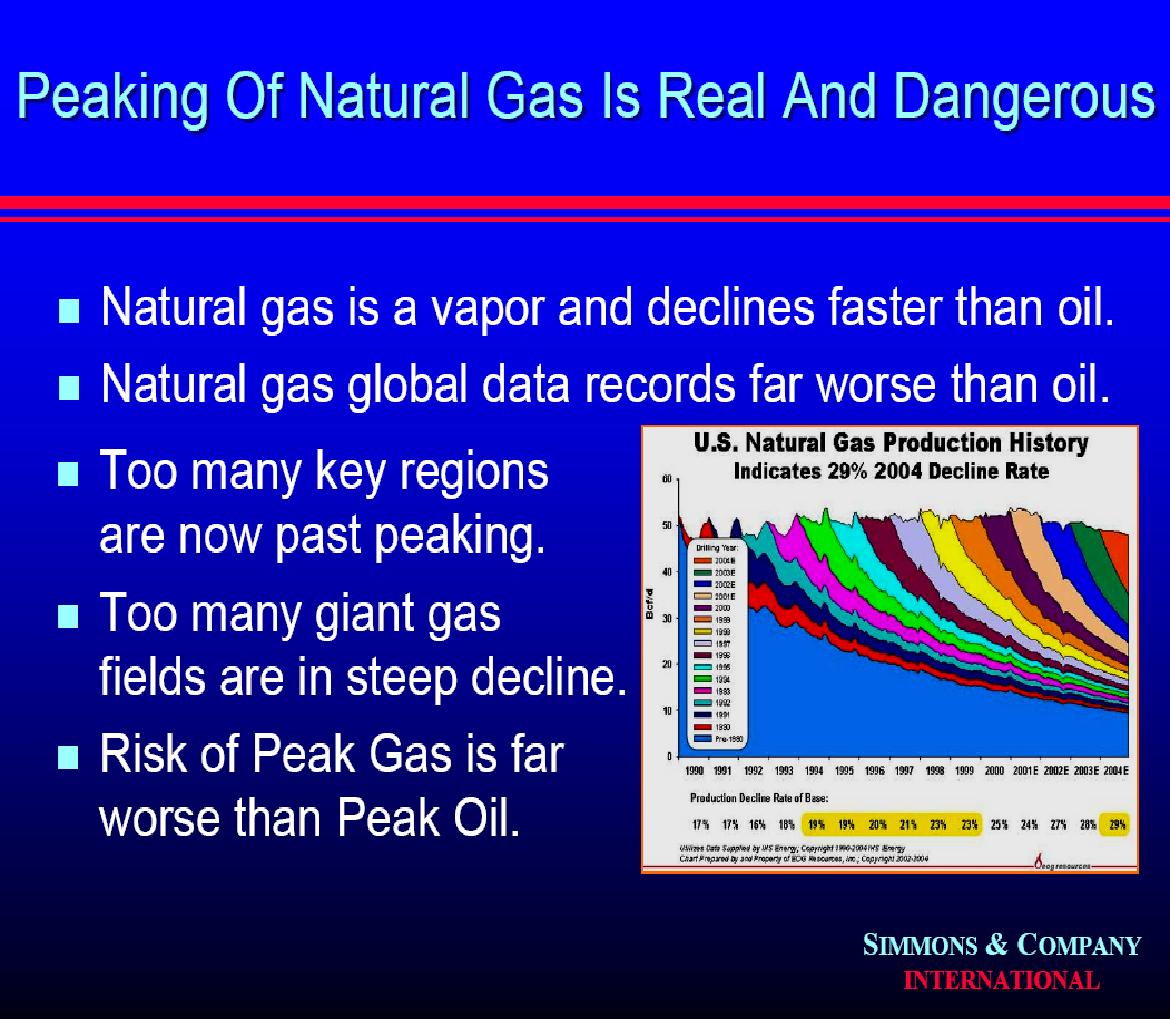

Here's a more recent edition of the IHS image on base decline rates for natural gas. It shows a base decline rate of 32%, which is up from the one I have for 2003 at 28%.

It looks drammatic - but what does it show? On decline charts, it is the band with tapering with time that counts and I sure as hell can't work that out from this. Also need somehow to overlay no. of wells drilled to see declining return on investment.

CW

It shows that the average well 15 years ago, starting with 50 bcf, would be down to 10 bcf today. But the average current well today is depleting at 32% a year - so will be dry (or close) to dry much much quicker than it used to. Some new wells drilled in Texas are empty in 9 months.

The definition of a treadmill. Coal bed methane has longer depletion profiles but are expensive because you have to get the water out first. Look at my previous nat gas post and you can see no. of wells drilled as well (though my graphics skills were poorer)

It looks like the base decline rate is increasing about 1%/yr too. At that rate, by 2025ish we'd have to replace half our production in just one year in order to keep production from declining.

Am I reading this plot wrong or is it kinda frightening? If this was the world oil situation we'd have to replace .32x85mbd = 27.2 mbd this year to keep production flat. How long can we keep replacing that amount of production every year?

Btw, I just started posting a few days ago, but I've been a lurker for some time.

@Nate- You can find the image at EOG Resources, here.

@CryWolf- As I remember, the "production decline rate of base" at 32% was explained to mean that if U.S. production stopped right now, then in one year U.S. production could be expected to drop 32% from its present level.

I interpreted the graph to show that each new year's production decline rates are steeper year after year; and cumulative decline rates on producing fields also are increasing; and that fit my understanding of the underlying dynamic much as described by oilmanbob above.

Anyone is welcome to correct me, or otherwise clarify.

The unconventional gas reserves mentioned above as shale gas and coal bed methane have lower initial production and drop off similarily, but the gas is economic much longer because the gas is seeping out of "tight" formations. The barnett shale wells in the Newark field are projected to las 30 years at 1/4th of the initial potential, with a refracking every 5 years or so. The fracturing jobs are huge-10,000 barrels of water or more-and can cost as much as drilling the well.

At any rate, because of the high decline rate of gas wells I expect any softness in the natural gas market will be firmed up after a few months of a drilling slow down, especially if we have a cold winter and/or a hot summer. And since around 15% of the gas consumed in the US comes from the Gulf, a big hurricane in the northern Gulf could cause a big spike.

Anyway, I learned alot from this post. After seeing the IHS graph I went back and read it more carefully. Thanks.

What's one and one and one and one and one and one and one and one and one and one?

I hope national prioritization of sensible uses of natural gas happens soon.

Great post, Nate, thanks!

Case in point: Panda Ethanol

1628 EST [Dow Jones] - Panda Ethanol Inc. signaled its intention this week to build a 100 million gallon-per-year ethanol plant near the city of Muleshoe, Texas, using cattle manure to generate the steam used in the ethanol manufacturing process, according to a news story posted on Agriculture.com.

The completed facility will annually refine approximately 38 million bushels of corn into the biofuel and will gasifying more than 1 billion pounds of cattle manure yearly. The Muleshoe facility is the sixth, 100-million gallon ethanol project announced by Panda, and the fourth to be powered by cattle manure. The company has received air permits for three of its six announced ethanol projects, according to Agriculture.com. (DMC)

www.defendscience.org

Peak Oil = Liquid Transportation Fuels crisis, not a heating homes crisis.

This morning the [NOAA http://www.cpc.ncep.noaa.gov/products/analysis_monitoring/enso_advisory/} issued a forecast for continued El nino conditions which typically favor a warmer climate in general particularly in NorthEast.

If we have another mild winter, on top of record storage, even the small (at this point) supply depletion will not stem the tide of natural gas sellers. This is why I believe our government (and others) should recognize this as a long term problem and put a price floor on natural gas (and oil too for that matter). This will provide incentive for alternative energy to compete and keep it there.

They could then take the excess gas (since storage would be full) and turn it into some intermediate product like ammonia for fertilizer or some other. (Totoneilas idea).

Market wont solve it, unless we get the exact combination of medium winters and medium summers to have gradual price increase or 300 LNG tankers miraculously appear

Leanan is right. Hot summer cold winter big trouble.

From a guy named 'Stan'

Just thought I would post a few of my observations for you guys while I was at it. I work in the oil industry as a contractor, mainly working in the field in northern BC, northern AB and rarely the NWT. There are a lot of guys like me who work a potion of the year in the field, usually in 2-4 week bursts and then spend the rest of the time at home in the lower mainland. I have been doing this for more than 10 years and have seen my fair share of boom and bust.

Currently we are heading for a bust. What many people are not aware of is that western canada is mainly a natural gas play with good pockets of heavier oil. Lots of the oil drilling in the last 2 years has been heavy (api <15) oil, such as in the peace river and wabasca areas. These wells were economic when oil was above $40 or so. However due to the labour squeeze, a lot of contractors and suppliers have ramped up their costs dramatically. Daily costs on a large rig are up to $85-100k from $65-75k a couple of years ago. In light of this many of the heavier oil plays are now marginal and investment is slowing. Meanwhile the price of natural gas has softened dramatically from $12 2 years ago whilst the operators have suffered the same cost increases. I have noticed over the last 3 months that some of the bigger nat. gas operators have colluded to try and starve some of the worst offenders in jacking up their rates. Devon, CNRL and Encana have slashed their drilling budgets and are releasing up to 50 rigs between them that were previously contracted long term. Presumably these rigs will be picked up by other operators, but this is feeling like a real slowdown to me. This has reduced the rig count of each operator by half. Bear in mind that the short term rush of jan and feb last year when every available rusting hulk was pressed into service the record rig count was around 860, (summers are 400-550), so you can see that a drop of 60 rigs on year round contract is significant. So far you will read none of this in the press, but it is certainly starting to be whispered in hushed tones around water coolers all over alberta. Many of the guys I work with have never experienced a slow down and will not even entertain the idea that it is possible. A lot of them earn huge money, but are real consumers and still manage to spend it well in advance. One guy I know earns approx $275k a year (you really have to sell your soul and work 280 days a year), but has monthly outgoings of $10k (house, f350, navigator for her, atv, quad, 12k plasma etc) why a guy like this needs to get a plasma on credit is beyond me but it is the pervading attitude of the industry. I realise that this is a dramatic example but it best highlights the attitudes of people in this industry.

http://www.caodc.ca/rigcounts.htm#biwkserv

Plots rig count for last 8 years or so. Note that it plots rigs up and down, so total is #rigs available for service.

Building a Better Fire

Maybe if they could use all the bull shit in Washington...

The steep drop in industrial use is explained by the de-industrialization of America and the substitution of domestic goods with imports.

How can we explain the drop in residential use? After all, the overall population is expanding and the number of new homes increasing. Two reasons:

a) Population is shifting dramatically to temperate climate zones (South and Southwest), requiring much less heating. Indeed, new home construction over the past few years was heavily concentrated there.

b) In many of those areas homes must be all-electric (heating, A/C, cooking). The large increase in gas use for peak load electricity production, also shown in the graph, makes this pretty clear.

Indeed, this graph shows we have an electricity supply problem and that is why power companies are planning to build coal-fired plants at a furious pace. As those come on-line gas demand will decline sharply.

By the way, another factor that will curtail overall gas demand is the current bust in housing. This was essentially the last bastion of large scale, energy intensive "manufacturing" in the US and had generated most of the economy's growth.

Therefore, I think we are heading for significantly lower overall demand in the coming years, although it may be that "excess" gas will be used for the production of oil from tar sands.

www.greencarcongress.com/2006/10/honda_natural_g.html

Industrial consumption, otoh, is logically falling fast because fertilizer and petrochemical plants are shutting down here as we increase our energy imports by importing these items where we used to produce them here. I see this component as providing a ceiling on prices until the collapse of US ng production around 2010-12.

The key to the Canadian NG supply situation is:

- when does the Arctic gas come onstream, and how much of it is there?

We are talking Alaska North Slope, Mackenzie Delta and the Canadian Islands in this.

I haven't done the homework. My sense is the pipeline is probably not finished before 2020, but in a 'scram' scenario, as my father points out, it could be done by 2012 (based on the WWII example, when the northern oil pipeline was built in 2 years).

(first time I viewed you asking a question - usually youre providing answers...;)